We offer clarity, common sense and total reliability, combined with financial flair.

We will be there for you when you need us with day-to-day issues and your financial administration will be managed proactively by your Client Manager

On Tuesday the Office for National Statistics (ONS) published the monthly public sector borrowing data for March 2024. After the Financial Times had reported at the weekend that the Chancellor was contemplating another NICs cut before the election, the numbers were a surprise. The first cut of the data for 2023/24 show:

The public sector net deficit ex banks (PSNB ex) in March 2024 is estimated to have been £11.9bn, meaning it was:

£4.7 less than a year ago;

£5.0bn more than in March 2022;

£13.6bn less than in March 2021;

£0.3bn below the OBR’s November monthly profile projection; and

£1.7bn above the Reuters economists’ median forecast.

Borrowing in 2023/24 provisionally amounts to £120.7bn (4.4% of GDP), £7.6bn less than in 2022/23. However, it is £6.6bn above the OBR’s revised 2023/24 forecast total, issued alongside last month’s Budget.

The latest estimate of total borrowing for the 2022/23 was revised up by £0.3bn to £128.3bn. It is now £10.9bn below the initial year end estimate, a reminder that over time data can be subject to significant revisions.

Overall public sector net debt excluding banks (PSND ex) was £2,694.2bn, equivalent to 98.3% of GDP (up 0.8% on a revised February figure). A year ago the figure was 97.6%.

When the Prime Minister made reducing the debt/GDP ratio one of his five pledges in early March 2023, the latest published ratio (for December 2022) was 95.8%, based on the March 2024 update of ONS calculations. The ratio keeps rising because debt is growing faster than GDP.

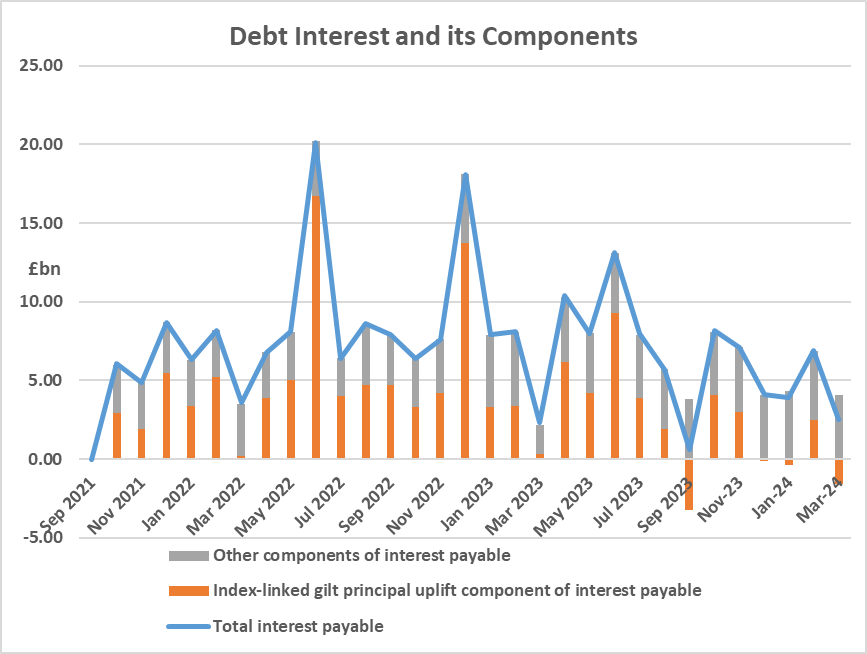

At £2.5bn, March 2024 interest payments were £4.4bn lower than February’s revised figure, and £0.2bn higher than a year ago. January’s negative contribution from the RPI, was repeated in March, with a £1.6bn downward revaluation of index-linked debt.

Total interest in 2023/24 provisionally amounts to £78.5bn, about 2.9% of GDP.

Total interest in 2023/24 provisionally amounts to £78.5bn, about 2.9% of GDP.

Bank of England holdings of gilts (at redemption value) fell by £4.3bn to £625.4bn. The gap between the reserves the Bank created to purchase the gilts under QE and their redemption value fell to £102.7bn (counted as government debt, as the Treasury indemnified the Bank against losses).

The OBR’s commentary on the figures notes that the £6.6bn overshoot of the OBR’s Budget forecast is largely driven by the first full-year estimate of central government receipts from the ONS, which is £5.3 billion lower than the OBR March forecast. The OBR says this figure is likely to be revised as additional data becomes available (see the change in 2022/23 deficit mentioned above, for example).

Rather than look at monthly movements in the cash receipts data as it usually does, this month the OBR compares its Budget projection against the ONS’s initial estimates for 2023/24 and makes the following points:

Accrued PAYE income tax and NICs receipts were £4.5bn (1.1%) lower than expected. The OBR thinks this is likely to primarily reflect weaker-than-expected bonuses, particularly from the financial sector. However, the figure could change as around half of bonuses in the December-to-March bonus season are paid out in March with the tax largely received in April.

Accrued receipts of onshore and offshore corporation tax were £1.5bn (1.5%) above the March estimate. The OBR expects this estimate is likely to be revised down in future, once March Economic and Fiscal Outlook (EFO) forecast information is incorporated.

Accrued VAT receipts were £0.8bn (0.5%) lower than forecast in March. This figure will also be subject to revision as some cash receipts received between April and June relate to spending at the start of 2024 and so will be accrued back to 2023/24.

Other central government receipts were £2.1bn lower than forecast in March, largely driven by interest and dividends receipts (£1.2bn below forecast) and lower central government depreciation (£0.9bn below forecast).

Lower debt interest spending (£3.9bn, or 4.7% below forecast), was due to lower-than-expected inflation in January. However, this is a provisional estimate that may be revised in future months.

Higher subsidies (£3.2bn or 11.1 % above forecast), largely reflect a £2.5bn upwards revision to the ONS’s estimate of spending on the contracts for difference scheme for electricity pricing. The OBR says this revision was neutral for borrowing, as there was a corresponding increase in central government receipts.

There was higher net investment than forecast (£1.1bn or 1.9% above forecast).

COMMENT

Unless future revisions come to his aid, the £6.6bn borrowing overshoot may have scuppered the chances of Mr Hunt holding another fiscal event before the polls open. Think back to the Budget and the Chancellor only met his fiscal rule of debt falling as a percentage of GDP five years out by £8.9bn. The thinness of that margin is well demonstrated by today’s data.

With the numbers going in the wrong direction and ten weeks’ notice required for the OBR to produce its next EFO, Mr Hunt might choose to leave its delivery until after the election.

Source: Techlink Professional

Essential Wealth Management

1-2 Great Farm Barns

West Woodhay

Newbury

Berkshire RG20 0BP

Tel: 01488 669840

Fax: 01488 669216

Email: [email protected]

Essential Wealth Management is a trading style of Essential Wealth Management and Advice Ltd, registered in England Number 04020006. Registered Office: 1-2 Great Farm Barns, West Woodhay Newbury, Berkshire, RG20 0BP. Essential Wealth Management and Advice Ltd is an appointed representative of The Openwork Partnership, a trading style of Openwork Limited which is authorised and regulated by the Financial Conduct Authority.

The information on this website is subject to the UK regulatory regime and is therefore targeted at consumers in the UK.

Approved by the Openwork Partnership on 18.04.2024