Commentary from Quilter Cheviot who manage some of our discretionary investment portfolios:

With a recession expected in the US and Europe, many investors are now questioning what will happen to company dividend payments, which some may rely upon to provide an income. While we are in the early stages of the pandemic and there is significant uncertainty around how large the economic impact will be, there are some initial conclusions we can draw to help income investors.

How far could dividends be cut?

From a high level perspective, dividends typically fall between 5-10% in a recession. In the Global Financial Crisis of 2008, we saw European dividends cut by about 30%. This was partly because the banking sector, a big payer of dividends, was at the epicentre of the crisis and was severely affected by the crisis and regulation to prevent it from reoccurring.

Some sectors will be affected more than others

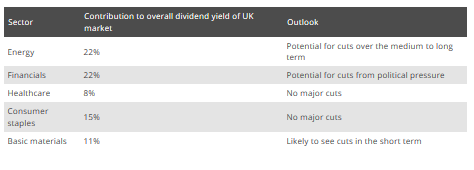

Dividends are most likely to be cut or suspended in the retail, travel and leisure industries, where quarantines across much of the UK, Europe and the US have naturally led to consumers staying at home rather than eating out, shopping or going on holiday. The below table provides a high level summary of the key FTSE 100 sectors and their dividend prospects.We have also seen a knock-on impact in related sectors such as property, with the tenants of many shopping centre landlords withholding rent. One shopping centre landlord has reportedly received only 25% of the rent from a shopping centre property to the end of March. Without going through each property landlord’s list of tenants, it is difficult to say how big an issue this might be. Landlords with mainly government tenants (e.g. Assura) or supermarket tenants (Supermarket Income REIT) should continue to pay out their dividend as normal however.

Questions over the energy and banking sectors

While the oil price has fallen by more than half from its recent highs, we do not believe oil producers such as BP or Shell will be under immediate pressure to cut their dividends, even if oil remains at $30 per barrel for some time. Oil producers are cutting investment in new projects and cancelling share buyback programmes, allowing them to free up cash and maintain their dividends.

The banking sector faces a different issue, with management teams worried that dividend payments will generate bad PR at a time when banks are under pressure to support small businesses and the wider economy. We have already seen some cuts from banks including Santander and Nordea.

The banking sector is well capitalised and in a much stronger position to weather any economic downturn than it was ten years ago. However, we would not be surprised if we saw at least some level of reduction in dividends, if only for public perception and for reasons of prudence if consumers and/or businesses default on their loans.

We would also note that dividends from European companies might be suspended or postponed for technical reasons. In Germany, for example, a company’s board normally proposes a dividend at the annual shareholder meeting, with shareholders voting on the proposal and the dividend then being paid out. However, these meetings normally require physical attendance, and it is unclear how the process will work whilst quarantines are in place.

Conclusion

Investors will likely need to adjust to reduced levels of income from existing portfolios, particularly in the UK where yields and pay-outs are normally higher. However, incremental investors can achieve very high yields in companies that we expect to keep increasing their payments. At present the UK stock market (FTSE 100) is yielding c. 6.8% compared to a long term average of 3.7%. Put another way, dividends could fall another 45% and would still trade on that average yield. The income produced by stocks still gives a lot of valuation support. Importantly, the differential between market yields (even assuming further cuts) and government debt has never been higher, providing some support for investors in the stock market today.