In order to ensure we provide our clients with the highest quality and breadth of service, we have a tried and tested team of associated professionals with specific fields of expertise.

The increase in the State Pension Age to 67 that begins next month. Why the justification now looks questionable.

We all know that the State Pension Age (SPA) is to increase to 67, starting in April 2026. But does it now make sense?

The announcement that the SPA would rise to 67 was made by George Osborne in November 2011 as part of his Autumn Statement. At the time, the SPA was 65 for men and a little under 62 for women. SPAs were due to equalise at 65 by late 2018 and then rise to 66 by October 2020. The document accompanying the Autumn Statement said:

“Since the life expectancy projections underpinning the original State Pension age timetable were published, average life expectancy at State Pension age in 2028 has increased by at least one and a half years for men and women. Given the ongoing increases in life expectancy beyond 2026, the Government will raise the State Pension age to 67 between April 2026 and April 2028.”

The further increase to 67 was expected to save around £60bn, in 2011 prices, between 2026/27 and 2035/36. In 2026 prices, that amounts to around £90bn, so, crudely, about £9bn a year. No doubt Rachel Reeves is grateful for her predecessor’s action, given the state of the Government’s finances.

However, the assumptions about life expectancy on which the change was introduced, by the Pensions Act 2014, appear overly optimistic with the benefit of hindsight:

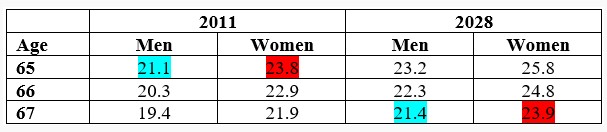

When the 2011 announcement was made, the Office for National Statistics (ONS) was just about to publish its 2010-based projections for life expectancy. These showed the following projected life expectancies for ages 65-67 in 2011 and 2028, when SPA would be 67:

The ONS view was thus that a 67-year-old in 2028 would have slightly higher life expectancy than a 65-year-old in 2011. If the yardstick was how many years would be spent in retirement, that justified the move to 67.

The ONS view was thus that a 67-year-old in 2028 would have slightly higher life expectancy than a 65-year-old in 2011. If the yardstick was how many years would be spent in retirement, that justified the move to 67.

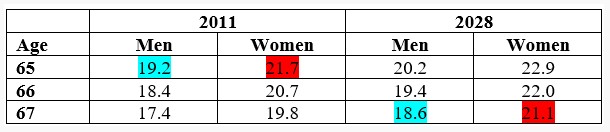

The latest ONS projections are 2022-based and were issued in February 2025. These show the following projections:

The latest ONS view is that a 67-year-old in 2028 would have 0.6 years’ lower life expectancy than a 65-year-old in 2011. The same set of projections suggests that the SPA should not rise to 67 until around 2035 if the aim is to match the life expectancy of a 65-year-old in 2011.

The latest ONS view is that a 67-year-old in 2028 would have 0.6 years’ lower life expectancy than a 65-year-old in 2011. The same set of projections suggests that the SPA should not rise to 67 until around 2035 if the aim is to match the life expectancy of a 65-year-old in 2011.

The difference between the two tables is explained by the ONS now taking a more pessimistic view about the pace of improvement in life expectancy, which has slowed markedly since 2010.

The previous and current Governments have held fast to the 2026-28 SPA increase and, in commissioning successive reviews of the move to an SPA of 68, made clear there would be no reassessment of the scheduling of the 67 SPA. The unspoken motivation was almost certainly financial.

Source: Techlink Professional. This is a news bulletin and is up-to-date as of the date of publishing. Please check the publishing date at the top of the article.

Essential Wealth Management

1-2 Great Farm Barns

West Woodhay

Newbury

Berkshire RG20 0BP

Tel: 01488 669840

Fax: 01488 669216

Email: [email protected]

Essential Wealth Management is a trading name of Essential Wealth Management and Advice Ltd which is an appointed representative of 2plan wealth management Ltd which is authorised and regulated by the Financial Conduct Authority. Essential Wealth Management and Advice Ltd is entered on the FCA register (www.FCA.org.uk) under no. 518528. Registered office: 1-2 Great Farm Barns, West Woodhay,Newbury, Berkshire RG20 0BP. Registered in England and Wales Number: 04020006.

The Financial Ombudsman Service is available to mediate individual complaints that clients and financial services businesses aren't able to resolve themselves. To contact the Financial Ombudsman Service please visit: http://www.financial-ombudsman.org.uk/contact/index.html

The information on this website is subject to the UK regulatory regime and is therefore targeted at consumers in the UK.

Approved by 2plan wealth management Ltd on 20/05/2025