In order to ensure we provide our clients with the highest quality and breadth of service, we have a tried and tested team of associated professionals with specific fields of expertise.

We offer clarity, common sense and total reliability, combined with financial flair.

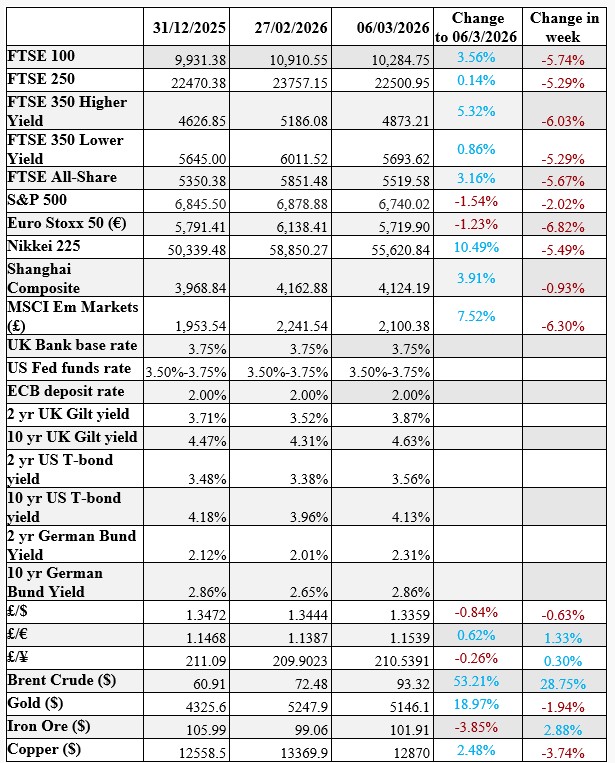

Market performance. The US/Israel-Iran war meant a volatile start to March. As ever, it is worth stepping back for some perspective.

The launch of a war against Iran by the US and Israel was always going to give investment markets jitters. In the run up to 28 February, the main evidence of fear had been the rise in the price of oil – Brent Crude was up 19% in the first two months of 2026. Other markets had generally been on a solid footing, with the Footsie posting a near 10% gain and Japan enjoying a 16.9% rise on the back of the election victory of Sanae Takaichi. Emerging markets were also buoyant, helped by strong AI-hardware related performance from Taiwan (+20.7%) and Korea (+44.9%). Ironically, the laggard was the USA, with the S&P 500 rising a mere 0.5% as the potential impact of AI rippled through various sectors of the market. Global bond yields fell across January and February on the expectation that there were more rate cuts to come later in the year. And then:

Across last week (2/3-6/3), equity markets took a hit, with many registering falls of 5%-6%. This time the US was the winner, although the S&P 500 was still down 2% on the week.

What has been overlooked somewhat in the panic is that, since the start of the year, most equity markets are still in positive territory, although the US once again is at the rear.

The picture for Government bonds is less rosy. Oil heading towards $100 a barrel and TTF gas prices up 67% in five days rekindled memories of the start of the Ukraine war and the inflationary leap which followed. Suddenly, prospects for central bank rate cuts turned to concerns about rate rises. That shows through a jump in two-year bond yields. The change was particularly notable in the UK, where, at the end of February, the expectation was for two more rate cuts by December. Ten-year bond yields also took a hit on the renewed inflationary concerns. The UK ten-year bond saw its largest weekly yield jump since the brief era of Liz Truss.

One surprising (non-) performance of the week was gold, which surged to over $5,400 an ounce on Monday only to end the week about $250 lower. Nevertheless, the shiny metal is still up 19% for the year to date.

Source: Techlink Professional. This is a news bulletin and is up-to-date as of the date of publishing. Please check the publishing date at the top of the article.

Source: Techlink Professional. This is a news bulletin and is up-to-date as of the date of publishing. Please check the publishing date at the top of the article.

Essential Wealth Management

1-2 Great Farm Barns

West Woodhay

Newbury

Berkshire RG20 0BP

Tel: 01488 669840

Fax: 01488 669216

Email: [email protected]

Essential Wealth Management is a trading name of Essential Wealth Management and Advice Ltd which is an appointed representative of 2plan wealth management Ltd which is authorised and regulated by the Financial Conduct Authority. Essential Wealth Management and Advice Ltd is entered on the FCA register (www.FCA.org.uk) under no. 518528. Registered office: 1-2 Great Farm Barns, West Woodhay,Newbury, Berkshire RG20 0BP. Registered in England and Wales Number: 04020006.

The Financial Ombudsman Service is available to mediate individual complaints that clients and financial services businesses aren't able to resolve themselves. To contact the Financial Ombudsman Service please visit: http://www.financial-ombudsman.org.uk/contact/index.html

The information on this website is subject to the UK regulatory regime and is therefore targeted at consumers in the UK.

Approved by 2plan wealth management Ltd on 20/05/2025