With effective planning and support, we can help you achieve your long-term financial goals.

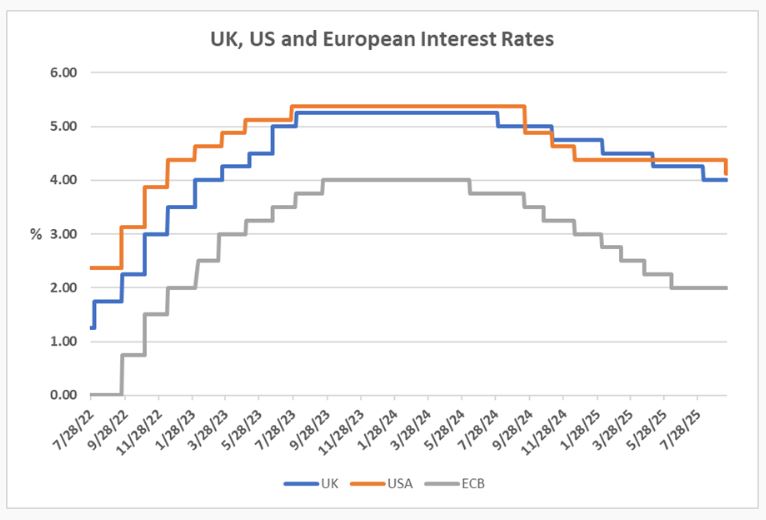

The Bank Rate. On Thursday, the Bank of England kept the Bank Rate at 4.0%, following the previous day’s widely-expected 0.25% cut from the Federal Reserve

In early August the Bank of England cut its Bank Rate by 0.25% to 4%, a week after the US Federal Reserve had held its Federal Funds Rate at 4.25%-4.50% for the fifth consecutive meeting. This week, it was the Bank’s turn to hold while the Fed brought out the secateurs.

In early August the Bank of England cut its Bank Rate by 0.25% to 4%, a week after the US Federal Reserve had held its Federal Funds Rate at 4.25%-4.50% for the fifth consecutive meeting. This week, it was the Bank’s turn to hold while the Fed brought out the secateurs.

The Fed’s move to 4.00%-4.25% had been widely anticipated. The central bank had been under relentless pressure from Donald Trump to reduce rates – to 1% is the President’s suggestion. Trump is primarily concerned about easing the cost of government borrowing (currently about $1.1trn a year), most of which is now being raised via Treasury Bills with terms of up to 12 months.

At the Fed, Jay Powell and Co were also having to react to a mix of sticky inflation numbers and disappointing employment figures. This was acknowledged in the Fed statement which noted “Job gains have slowed, and the unemployment rate has edged up but remains low. Inflation has moved up and remains somewhat elevated.” In contrast the July statement had said “The unemployment rate remains low, and labour market conditions remain solid. Inflation remains somewhat elevated.”

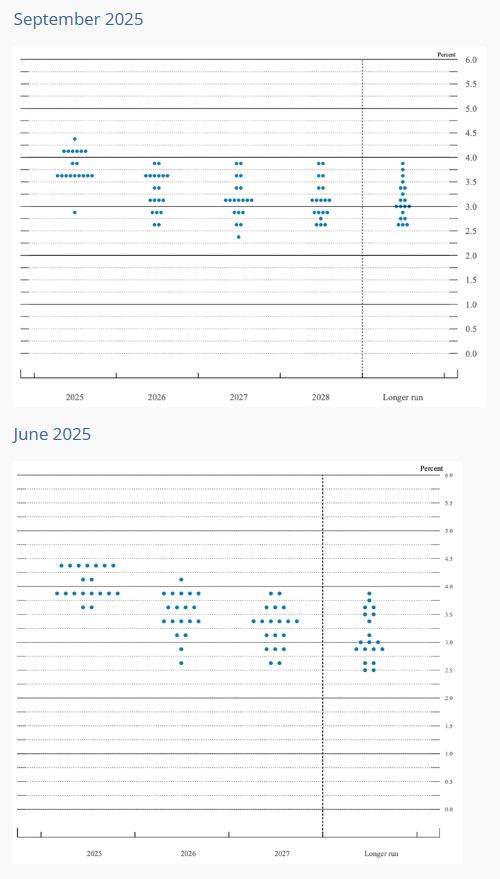

This meeting accompanied by a new dot-plot (see below) showing Fed members’ projections of future interest rates. The median projection was for another two 0.25% cuts by the end of the year, but this was distorted by one dot suggesting five more cuts (to 2.75%-3.00%) by December. It is assumed that this outlier belongs to Trump’s new temporary appointee to the Fed board, Steve Miran, who was the only dissenting member to favour of a jumbo 0.5% cut.

On this side of the Atlantic, the voting at Threadneedle Street moved back to its normal one-round pattern this month with seven Monetary Policy Committee (MPC) members voting in favour of holding rates and two preferring to see a 0.25% cut. In explaining the hold decision, the Bank said:

On this side of the Atlantic, the voting at Threadneedle Street moved back to its normal one-round pattern this month with seven Monetary Policy Committee (MPC) members voting in favour of holding rates and two preferring to see a 0.25% cut. In explaining the hold decision, the Bank said:

“Underlying disinflation has generally continued, although with greater progress in easing wage pressures than prices. Twelve-month CPI inflation was 3.8% in August, and is expected to increase slightly in September, before falling towards the 2% target thereafter. The Committee remains alert to the risk that this temporary increase in inflation could put additional upward pressure on the wage and price-setting process. Pay growth remains elevated, but has fallen and is expected to slow significantly over the rest of the year. Services consumer price inflation has been broadly flat over recent months. Upside risks around medium-term inflationary pressures remain prominent in the Committee’s assessment of the outlook.

Underlying UK GDP growth has remained subdued, consistent with a continued, gradual loosening in the labour market, as well as a margin of slack in the economy. Downside domestic and geopolitical risks around economic activity remain.”

The Bank of England does not offer anything approaching a dot plot, but it hinted at the potential for future rate cuts, saying:

“A gradual and careful approach to the further withdrawal of monetary policy restraint remains appropriate.”

However, in the best of balanced central bank wording it also added:

“The timing and pace of future reductions in the restrictiveness of policy will depend on the extent to which underlying disinflationary pressures continue to ease. Monetary policy is not on a pre-set path, and the Committee will remain responsive to the accumulation of evidence.”

Unsurprisingly, there was more than an echo of this stance in the Fed’s statement:

“In assessing the appropriate stance of monetary policy, the Committee will continue to

monitor the implications of incoming information for the economic outlook. The Committee

would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that

could impede the attainment of the Committee’s goals.”

Arguably the more significant decision the MPC took at its meeting was how much quantitative tightening (QT – unwinding of quantitative easing) to undertake over the next 12 months.

Source: Techlink Professional

This is a news bulletin and is up-to-date as of the date of publishing. Please check the publishing date at the top of the article.

Essential Wealth Management

1-2 Great Farm Barns

West Woodhay

Newbury

Berkshire RG20 0BP

Tel: 01488 669840

Fax: 01488 669216

Email: [email protected]

Essential Wealth Management is a trading name of Essential Wealth Management and Advice Ltd which is an appointed representative of 2plan wealth management Ltd which is authorised and regulated by the Financial Conduct Authority. Essential Wealth Management and Advice Ltd is entered on the FCA register (www.FCA.org.uk) under no. 518528. Registered office: 1-2 Great Farm Barns, West Woodhay,Newbury, Berkshire RG20 0BP. Registered in England and Wales Number: 04020006.

The Financial Ombudsman Service is available to mediate individual complaints that clients and financial services businesses aren't able to resolve themselves. To contact the Financial Ombudsman Service please visit: http://www.financial-ombudsman.org.uk/contact/index.html

The information on this website is subject to the UK regulatory regime and is therefore targeted at consumers in the UK.

Approved by 2plan wealth management Ltd on 20/05/2025