With effective planning and support, we can help you achieve your long-term financial goals.

How an individual’s tax position will increase as a result of up-coming tax rate rises.

With increases in the dividend tax rate for basic and higher rate taxpayers from 6 April 2026 and further increases for savings and property income for basic, higher and additional rate taxpayers from 6 April 2027, we look at how an individual’s tax position will increase.

From 6 April 2026, dividend income will be taxed at 10.75% from 8.75% for basic rate taxpayers and 35.75% from 33.75% for higher rate taxpayers. The rate for additional rate taxpayers will remain at 39.35%. There will be no change to the dividend allowance which remains at £500 per person.

In addition, from 6 April 2027, savings income and property income will be taxed at 22% from 20% for basic rate taxpayers, 42% from 40% for higher rate taxpayers and 47% from 45% for additional rate taxpayers.

Remember the personal savings allowance for a basic rate taxpayer is £1,000 and £500 for a higher rate taxpayer. An additional rate taxpayer is not entitled to a personal savings allowance.

In this bulletin we look at some examples of how an individual’s tax position will change in light of these increased rates.

Case study 1

Cara works part-time in a bakery earning £15,000. A few years ago, she inherited a share portfolio from her late uncle which generates £4,250 in dividends. She also receives bank interest of around £676.

After taking account of her personal allowance, personal savings allowance and dividend allowance her taxable income would be as follows:

Earned income - £15,000 - £12,570 = £2,430

Bank interest £676 - £676 = £0

Dividend income £4,250 - £500 = £3750

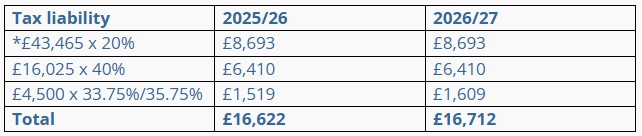

Case study 2

Case study 2

Cliff has a salary of £72,060 and receives dividends of £5,000 from his share portfolio. Cliff is a member of his workplace group personal pension scheme. His employer pays 8% of his salary into his pension and Cliff also pays 8%.

His taxable income will be as follows:

Earned income £72,060 - £12,570 = £59,490

Dividend £5,000 - £500 = £4,500

*Basic rate tax band £43,465 (£37,700 + £5,764.80 [£72,060 x 8%])

*Basic rate tax band £43,465 (£37,700 + £5,764.80 [£72,060 x 8%])

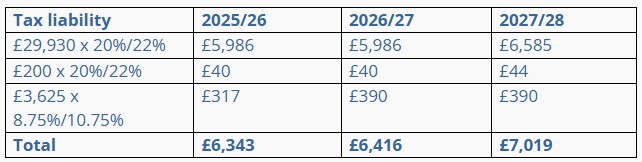

Case study 3

Jay has built up a property portfolio which provides him with rental income, after allowable expenses, of £42,500. His own property is mortgage free. He also receives bank account interest of £1,200 and dividends of £4,125. After taking account of his allowances, his taxable income will be as follows:

Rental income £42,500 - £12,570 = £29,930

Bank interest £1,200 - £1,000 = £200

Dividends £4,125 - £500 = £3,625

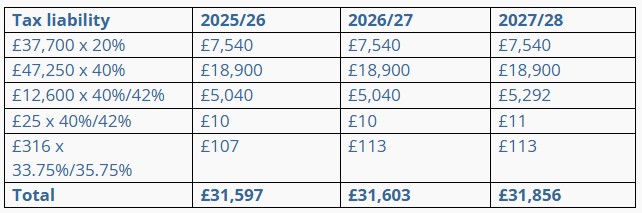

Case study 4

Case study 4

Damian earns £93,700. His other income comprises, bank account interest of £525, dividend income of £816 and rental income, after allowable expenses, of £12,600.

As his total income is £107,641 he would lose part of his personal allowance.

£107,641 - £100,000 = £7,641/2 = £3,820.50

£12,570 - £3,820 = £8,750

His taxable income would therefore be as follows:

Earned income £93,700 - £8,750 = £84,950

Rental income £12,600

Bank interest £525 - £500 = £25

Dividends £816 - £500 = £316

Source: Techlink Professional. This is a news bulletin and is up-to-date as of the date of publishing. Please check the publishing date at the top of the article.

Source: Techlink Professional. This is a news bulletin and is up-to-date as of the date of publishing. Please check the publishing date at the top of the article.

Essential Wealth Management

1-2 Great Farm Barns

West Woodhay

Newbury

Berkshire RG20 0BP

Tel: 01488 669840

Fax: 01488 669216

Email: [email protected]

Essential Wealth Management is a trading name of Essential Wealth Management and Advice Ltd which is an appointed representative of 2plan wealth management Ltd which is authorised and regulated by the Financial Conduct Authority. Essential Wealth Management and Advice Ltd is entered on the FCA register (www.FCA.org.uk) under no. 518528. Registered office: 1-2 Great Farm Barns, West Woodhay,Newbury, Berkshire RG20 0BP. Registered in England and Wales Number: 04020006.

The Financial Ombudsman Service is available to mediate individual complaints that clients and financial services businesses aren't able to resolve themselves. To contact the Financial Ombudsman Service please visit: http://www.financial-ombudsman.org.uk/contact/index.html

The information on this website is subject to the UK regulatory regime and is therefore targeted at consumers in the UK.

Approved by 2plan wealth management Ltd on 20/05/2025