Our holistic approach, combined with an insightful understanding of the worlds of finance, law, taxation, investment and insurance, ensures all your bases are covered.

Nearly all our clients are referred by existing clients, a testament to our service.

Ahead of its Green Budget presentation on Thursday, the Institute for Fiscal Studies (IFS) has issued the Green Budget chapter examining tax increase options.

Source: IFS

Source: IFS

The big pre-Budget event for the Institute for Fiscal Studies is its Green Budget Presentation on Thursday 16 October. Ahead of that, on Monday it published the Green Budget chapter entitled ‘Options for Tax Increases’. If you are looking for a shopping list of tax hikes, as the Resolution Foundation provided, you will not find it here. The IFS has taken a more theoretical view of what Rachel Reeves might consider, given her constraints.

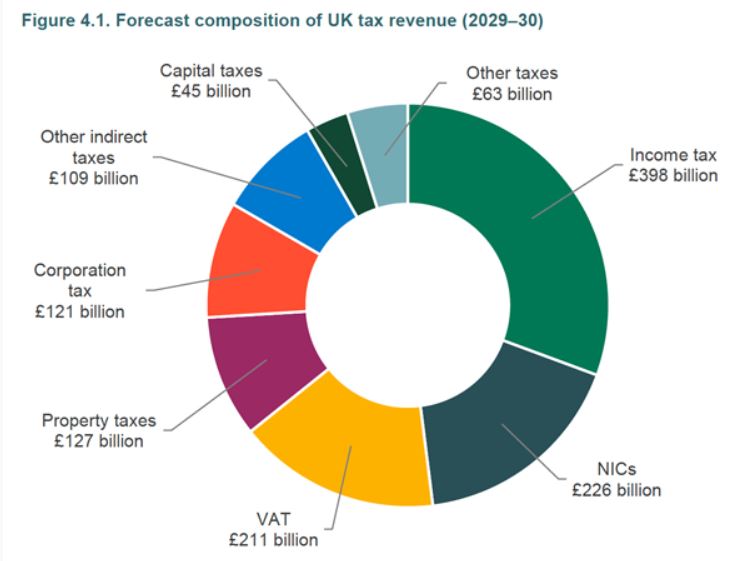

The chapter starts with consideration of the currently expected revenues from various taxes in 2029/30, the crucial year for the Chancellor’s ‘stability rule’. The chapter’s key findings are:

Tax revenue as a share of national income is set to reach a UK record high of 37.4% in 2026/27. The IFS repeats a point it has made before that this tax share is lower than in many other Western European countries, implying that it would be feasible for the Chancellor to raise more tax revenue if desired.

Raising the rates of income tax, National Insurance contributions (NICs) or VAT – the three largest taxes – could straightforwardly raise large sums. Together the trio raise about two thirds of all revenue (see chart above), but any change to them risks breaking Labour’s manifesto promise not to “increase National Insurance, the basic, higher, or additional rates of Income Tax, or VAT”. For the record – and underlining the government’s self-imposed constraint – the IFS estimates that by 2029/30:

- Increasing all rates of income tax by one percentage point would yield £10.9bn a year.

- Increasing individual (i.e. employee and self-employed) and employer rates of NICs by one percentage point would yield £14.5bn a year.

- Increasing the main rate of VAT by one percentage point would yield £9.9bn a year.

In common with other think tanks, the IFS says that extending the ongoing freeze in personal tax thresholds would also raise a significant amount (£10.4bn a year by 2029/30) but suggests that if the freeze included NICs thresholds it would arguably also break the manifesto pledge. As ever, the IFS is critical of a tax rise that is “determined by the vagaries of future inflation.”

A new tax on income, hypothecated to a particular spending stream, may be a more politically attractive way to increase tax on a large tax base, but would add unnecessary complexity to the tax system. The idea here echoes Rishi Sunak’s short-lived Health & Social Security Levy, a de facto NICs increase. The IFS says hypothecation would either be unjustifiably restrictive or economically meaningless.

Restricting income tax relief on pension contributions would raise large sums but should be avoided. The IFS believes it would be unfair and distortionary to restrict up-front relief but continue to tax pension income at the taxpayer’s marginal rate. It makes the familiar point that it would also be practically very difficult to attribute employer contributions to defined benefit arrangements to specific individuals so that they could be taxed. The IFS’s preferred options for increasing tax on pensions include levying some NICs on employer pension contributions and/or reforming the 25% tax-free element of pension income.

Raising significantly more revenue from the four largest taxes after the manifesto’s untouchable trio – corporation tax, council tax, business rates and fuel duties – would also bring challenges. On corporation tax, the government’s own roadmap is a block, while for council tax and fuel duties, the OBR forecasts already incorporate significant increases (4.3% a year council tax rises and for fuel duty reinstatement of RPI-linked duty rises and abolition of the 2022 5p ‘temporary’ reduction). While a doubling of English council tax for bands G and H (4% of all properties) would raise £4.2bn by 2029/30, the IFS offers the reminder that it would remain a tax based on 1991 property values, so be poorly targeted.

For business rates, the government’s steer so far has been tweaks that are revenue neutral (eg shifting some business rates from small retail properties to large properties). Here, the IFS reiterates its call for serious reform in the guise of a land value tax for commercial property.

Simply raising tax rates on income from capital – including rental income, dividends, interest and self-employment profits – could raise money but would discourage saving and investment. The IFS returns to the plea it has made in earlier reports for ‘genuine reform’ rather than more revenue-motivated tinkering. It wants to see improvement to the design of the tax base (entailing some giveaways) and closer alignment of overall tax rates across different forms of income and gains. In this respect it echoes comments from many other think tanks.

An annual wealth tax would face huge practical challenges. The IFS is no fan of a wealth tax, believing it would also penalise saving and, the more it was concentrated on the very wealthy, the more it would incentivise them to leave (or not come to) the UK. A better solution in the IFS’s view would be well-functioning taxes on capital income and gains. This would include, for example, abolishing CGT rebasing on death (worth £2.3bn a year by 2029/30, the IFS estimates).

The Chancellor should not increase stamp duties or insurance premium tax. The SDLT argument follows that set out in our recent Bulletin on the Conservative proposals for limited abolition. On insurance premium tax (worth £9.2bn in 2025/26), the IFS case is that the tax has morphed from being a substitute to VAT on insurance to a tax which now creates damaging distortions to production decisions.

The tax gap for small companies has ballooned and reducing it should be a priority. While the overall tax gap (between taxes owed and revenues collected) has fallen (to an HMRC-estimated 5.3% in 2023/24), the small companies’ gap has ballooned to 40%, again according to HMRC. As the IFS notes, that equates to £24bn by 2029/30. Returning the gap to its 2017/18 level would be the equivalent of raising £10bn.

Source: Techlink Professional. This is a news bulletin and is up-to-date as of the date of publishing. Please check the publishing date at the top of the article.

Essential Wealth Management

1-2 Great Farm Barns

West Woodhay

Newbury

Berkshire RG20 0BP

Tel: 01488 669840

Fax: 01488 669216

Email: [email protected]

Essential Wealth Management is a trading name of Essential Wealth Management and Advice Ltd which is an appointed representative of 2plan wealth management Ltd which is authorised and regulated by the Financial Conduct Authority. Essential Wealth Management and Advice Ltd is entered on the FCA register (www.FCA.org.uk) under no. 518528. Registered office: 1-2 Great Farm Barns, West Woodhay,Newbury, Berkshire RG20 0BP. Registered in England and Wales Number: 04020006.

The Financial Ombudsman Service is available to mediate individual complaints that clients and financial services businesses aren't able to resolve themselves. To contact the Financial Ombudsman Service please visit: http://www.financial-ombudsman.org.uk/contact/index.html

The information on this website is subject to the UK regulatory regime and is therefore targeted at consumers in the UK.

Approved by 2plan wealth management Ltd on 20/05/2025