With effective planning and support, we can help you achieve your long-term financial goals.

In order to ensure we provide our clients with the highest quality and breadth of service, we have a tried and tested team of associated professionals with specific fields of expertise.

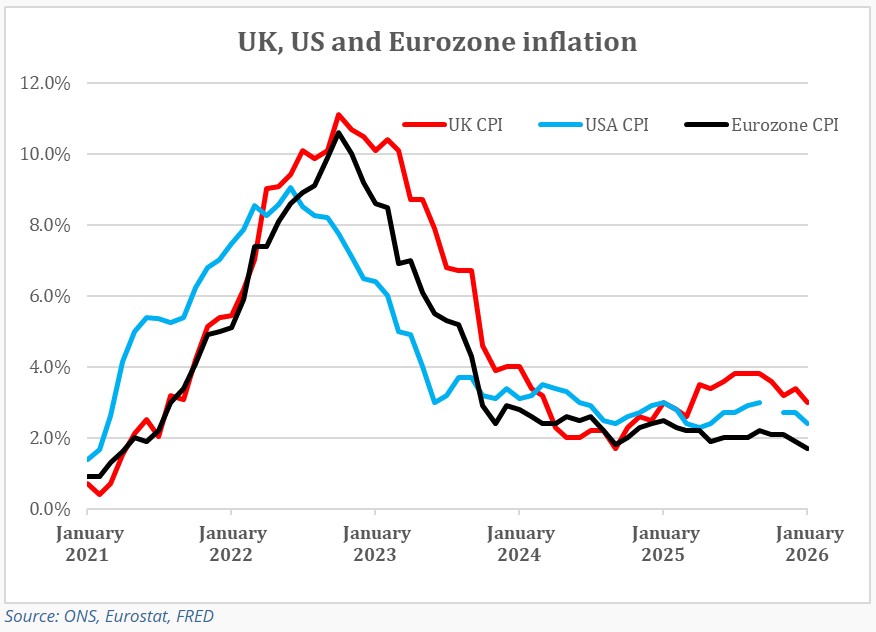

The UK CPI inflation rate for January 2026, which was 3.0%, down 0.4% from December 2025

Annual CPI inflation for January 2026 was down 0.4% from the previous month at 3.0%. A fall was widely expected with the market consensus expectation being for a figure of around 3%. In its February Monetary Policy Committee Minutes the Bank of England said, “CPI inflation was expected to fall back to around the 2% target from April. This mainly reflected developments in energy prices, including the impact of measures announced in Budget 2025.” This month, the Bank had projected a 2.9% reading for January 2026.

Annual CPI inflation for January 2026 was down 0.4% from the previous month at 3.0%. A fall was widely expected with the market consensus expectation being for a figure of around 3%. In its February Monetary Policy Committee Minutes the Bank of England said, “CPI inflation was expected to fall back to around the 2% target from April. This mainly reflected developments in energy prices, including the impact of measures announced in Budget 2025.” This month, the Bank had projected a 2.9% reading for January 2026.

The 3.0% CPI figure came after yesterday’s 4.2% earnings growth (both including and excluding bonuses) and 5.2% unemployment rate data. However, the earnings growth numbers need treating with caution as they remain distorted by a high reading (7.2%) for the public sector regular earnings, reflecting unusual timing of pay rises. This statistical quirk will drop out of the annual comparison over the next couple of months. Private sector regular pay rose by 3.4%.

The UK CPI reading was down 0.5% between December and January, whereas the corresponding period of 2025 saw a 0.1% decrease. The CPI/RPI gap was unchanged at 0.8% with the RPI annual rate also falling by 0.4% (to 3.8%). Over the month, the RPI index fell 0.5%.

The Office for National Statistics (ONS)’s favoured CPIH index completed the trio of 0.4% annual falls, with a January figure of 3.2%. As we have regularly said in recent months, a large part of that excess is due to the owner occupiers’ housing (OOH) category, which now has a 13.7% weighting in the CPIH (down from 17.1% in 2025) but is absent from the CPI. The OOH inflation rate dropped 0.3% to 3.9%, 4.1% off its peak January 2025 level and back to the level last seen in February 2023.

The ONS attributed the decline in CPIH inflation to:

Main downward drivers

Transport. Prices in this division rose overall by 2.7% in the 12 months to January 2026, down from 4.0% in the 12 months to December. On a monthly basis, prices fell by 1.8% in January 2026, compared with a fall of 0.5% a year ago.

The largest downward effect came from motor fuels, with both petrol and diesel prices falling between December 2025 and January 2026, whereas they rose in the corresponding period a year ago. Overall motor fuel prices dropped by 2.2% in the 12 months to January 2026, compared with a rise of 0.9% in the 12 months to December 2025.

The second-largest downward effect came from air fares, which tend to rise into December and fall into January. In December 2024 and January 2025, this pattern was less pronounced than in previous years, but December 2025 to January 2026 has reverted to normal. The ONS suggests that this might be because the return flights in December 2025 did not fall on Christmas Eve and New Year's Eve, a reminder of how sensitive CPI data can be to precisely when a price reading is made.

Food and non-alcoholic beverages. Prices in this division rose by 3.6% in the 12 months to January 2026, down from 4.5% in the 12 months to December 2025. On a monthly basis, food and non-alcoholic beverages prices fell by 0.1% in January 2026, compared with a rise of 0.9% a year ago. There were downward effects to the change in the rate from six of the eleven food and non-alcoholic beverages classes, with bread and cereals making the largest contribution.

Housing and household services. The 12-month inflation rate for housing and household services was 4.2% in January 2025, down from 4.6% in December. On a monthly basis, prices rose by 0.2% in January 2025, compared with a rise of 0.5% a year ago. The easing in the 12-month rate between December 2025 and January 2026 mainly reflected a continued downward effect from owner occupiers' housing (OOH) costs (please see above).

There was also an easing effect from gas, where prices fell by 2.7% in the 12 months to January 2026, compared with a rise of 2.1% in December 2025. However, the January Ofgem price cap change also introduced a counterbalancing upward effect from electricity, where prices rose by 5.3% in the 12 months to January 2026, compared with a rise of 2.7% in December 2025.

Education. Prices in the education division rose by 5.1% in the 12 months to January 2026, down from 7.6% in the 12 months to December 2025. On a monthly basis, prices were unchanged in January 2026, compared with a rise of 2.4% a year ago.

The downward contribution came entirely from private school fees, which rose by 12.7% a year ago after they became subject to Value Added Tax (VAT), and there was no change in price in January 2026.

Main upward driver

Restaurants and hotels. Prices in this division rose by 4.1% in the 12 months to January 2026, up from 3.8% in the 12 months to December 2025. On a monthly basis, prices fell by 0.7% in January 2026, compared with a fall of 1.0% a year ago.

The largest upward contribution came from the hotel item where prices are collected the night before the stay, with prices falling by 8.8% in January 2026 compared with a fall of 12.2% a year ago.

Six of the twelve broad CPI divisions saw annual inflation decrease, while four recorded a rise and two were unchanged. The categories with the highest annual inflation rate were Education (5.1%), Alcoholic beverage and tobacco (4.6%) and Communication (4.6%). Only one category, Furniture, household equipment and maintenance (-0.5%), recorded an annual fall.

Core CPI inflation (CPI excluding energy, food, alcohol and tobacco) fell 0.1% at 3.1%. Goods inflation fell 0.6% to 1.6%, while services inflation, a focus for the Bank of England, was down 0.1% at 4.4%.

The ONS restarted the issue of its Producer Price Inflation indices in September, but says that “The accredited official statistics status of these statistics is suspended, pending a review by the Office for Statistics Regulation.” With that caveat in mind:

Producer input prices fell by 0.2% in the year to January 2026, down from a revised rise of 0.5% in the year to December 2025.

Producer output (factory gate) prices rose by 2.5% in the year to January 2026, down from a revised 3.1% for December 2025.

Source: Techlink Professional. This is a news bulletin and is up-to-date as of the date of publishing. Please check the publishing date at the top of the article.

Essential Wealth Management

1-2 Great Farm Barns

West Woodhay

Newbury

Berkshire RG20 0BP

Tel: 01488 669840

Fax: 01488 669216

Email: [email protected]

Essential Wealth Management is a trading name of Essential Wealth Management and Advice Ltd which is an appointed representative of 2plan wealth management Ltd which is authorised and regulated by the Financial Conduct Authority. Essential Wealth Management and Advice Ltd is entered on the FCA register (www.FCA.org.uk) under no. 518528. Registered office: 1-2 Great Farm Barns, West Woodhay,Newbury, Berkshire RG20 0BP. Registered in England and Wales Number: 04020006.

The Financial Ombudsman Service is available to mediate individual complaints that clients and financial services businesses aren't able to resolve themselves. To contact the Financial Ombudsman Service please visit: http://www.financial-ombudsman.org.uk/contact/index.html

The information on this website is subject to the UK regulatory regime and is therefore targeted at consumers in the UK.

Approved by 2plan wealth management Ltd on 20/05/2025