Our holistic approach, combined with an insightful understanding of the worlds of finance, law, taxation, investment and insurance, ensures all your bases are covered.

With effective planning and support, we can help you achieve your long-term financial goals.

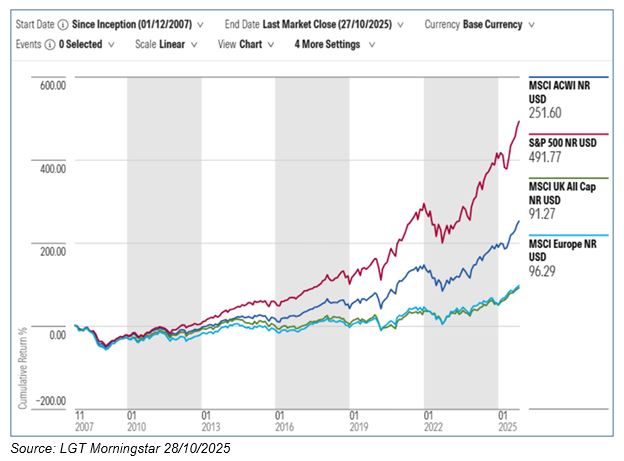

Uncertainty has defined the global economic landscape in 2025, with headlines and equity markets sending mixed signals all year. Warnings of recessions, global slowdowns in growth and deteriorating consumer and business confidence have been widely discussed and debated.

Yet equity markets, particularly the US, continue to reach new highs and market volatility has cooled thanks to recent inflation data. Fears of tariffs derailing markets have somewhat abated and Asia and emerging market equities have shown strength, supported by a weaker dollar. The optimism that equity markets are experiencing is underpinned by solid earnings and supportive liquidity conditions. However, given these diverging narratives, many investors are now asking, are markets too high? We believe the key to navigating this type of market is diversification and careful selection of fund managers.

Robust equity performance

Robust equity performance

Global equity markets have enjoyed strong performance, with the S&P 500 and other major indices hitting new record highs. The optimism is underpinned by solid earnings, constructive economic data, and the ongoing enthusiasm around artificial intelligence (AI). There have been significant flows into passive investments and ETFs which have elevated markets.

Markets have also been reacting to the possibility of a Federal Reserve (Fed) rate cut, which would shift monetary policy to a more stimulative stance rather than restrictive. Valuations are elevated with the S&P 500 trading at around 23× forward earnings, well above its long-term average of about 17×.

Market leadership has also been narrow, as the Magnificent 7 continue to dominate index performance. Given these factors, it is understandable some investors are concerned. This means diversification is as important as ever to ensure portfolios remain balanced between risky and defensive assets during this period.

Reasons to remain invested

Reasons to remain invested

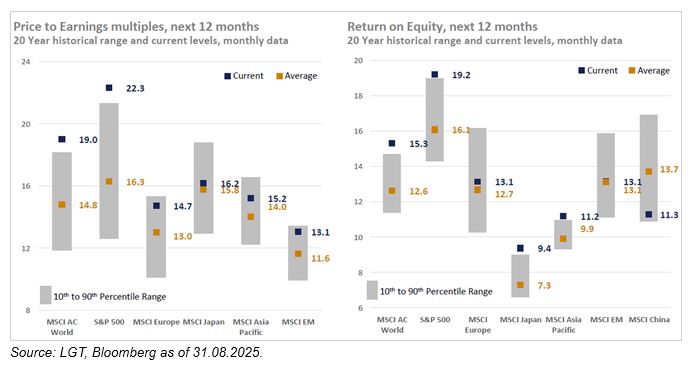

1. Earnings quality – you get what you pay for. Though US valuations do look lofty, earnings have backed up rising prices. And these two are not disconnected. The chart above shows the underlying earnings picture remains strong, and there are regions delivering genuine earnings growth. It also shows that many markets currently have high price-to-earnings multiples relative to their historical averages, but this is justified by higher-than-average return-on-equity.[1] So, while current valuations are elevated, so too are earnings and returns, suggesting that you are paying for quality. Our investment committee are keeping a close eye for any changes to this dynamic and we have recently downgraded our Valuation score of US equities within our Fundamentals, Valuations and Technicals (FVT) asset class framework to reflect the recent performance.

2. Balancing the Magnificent 7. Avoiding the Mag 7 comes with its own set of risks and the narrative can be hard to fight. Investment flows to these names, coupled with those previously mentioned strong earnings and demand for AI, means it can be quite a large risk to not hold them to weight. Our models are currently running with an underweight to Mag 7 vs ACWI, so whilst we maintain an exposure to these names, we’ve limited this allocation. We want to avoid a situation where all the eggs are in a Mag 7-shaped basket.

3. Economic data is more resilient than markets were expecting, unemployment remains low across major economies and global growth has proven to be stable. The levels of capital expenditure seen in the AI sector has helped support both growth and business confidence.

4. Monetary policy is shifting away from being restrictive. Fed Chairman Jerome Powell has signalled that the Quantitative Tightening cycle is ending, and markets are pricing in multiple rate cuts throughout 2026. This should provide a supportive environment for more economically sensitive assets.

5. China and US trade talks have added a layer of optimism for the region as investors hope to see both countries deliver a framework deal on tariffs. Any early threats of escalation between the countries are more likely being flagged as TACO “Trump Always Chickens Out”, and belief of compromises is lifting markets.

Source: LGT Wealth Management UK LLP

Essential Wealth Management

1-2 Great Farm Barns

West Woodhay

Newbury

Berkshire RG20 0BP

Tel: 01488 669840

Fax: 01488 669216

Email: [email protected]

Essential Wealth Management is a trading name of Essential Wealth Management and Advice Ltd which is an appointed representative of 2plan wealth management Ltd which is authorised and regulated by the Financial Conduct Authority. Essential Wealth Management and Advice Ltd is entered on the FCA register (www.FCA.org.uk) under no. 518528. Registered office: 1-2 Great Farm Barns, West Woodhay,Newbury, Berkshire RG20 0BP. Registered in England and Wales Number: 04020006.

The Financial Ombudsman Service is available to mediate individual complaints that clients and financial services businesses aren't able to resolve themselves. To contact the Financial Ombudsman Service please visit: http://www.financial-ombudsman.org.uk/contact/index.html

The information on this website is subject to the UK regulatory regime and is therefore targeted at consumers in the UK.

Approved by 2plan wealth management Ltd on 20/05/2025