Nearly all our clients are referred by existing clients, a testament to our service.

The UK stock market hit a record high amid hopes of an interest rate cut and easing political tensions

The FTSE 100 soared to a record high in April, lifted by hopes of interest rate cuts in the summer and easing tensions in the Middle East. UK shares were also buoyed by the brightening economic outlook, with inflation slowing and the economy returning to growth after a shallow recession at the end of 2023.

UK inflation eased from 3.4% in February to 3.2% in the 12 months to March – the weakest level for two and a half years. Some expect a sharp fall in the next inflation reading due to the year-on-year impact of energy prices. The latest figures are moving closer to the Bank of England’s 2% inflation target as it considers when to start cutting rates.

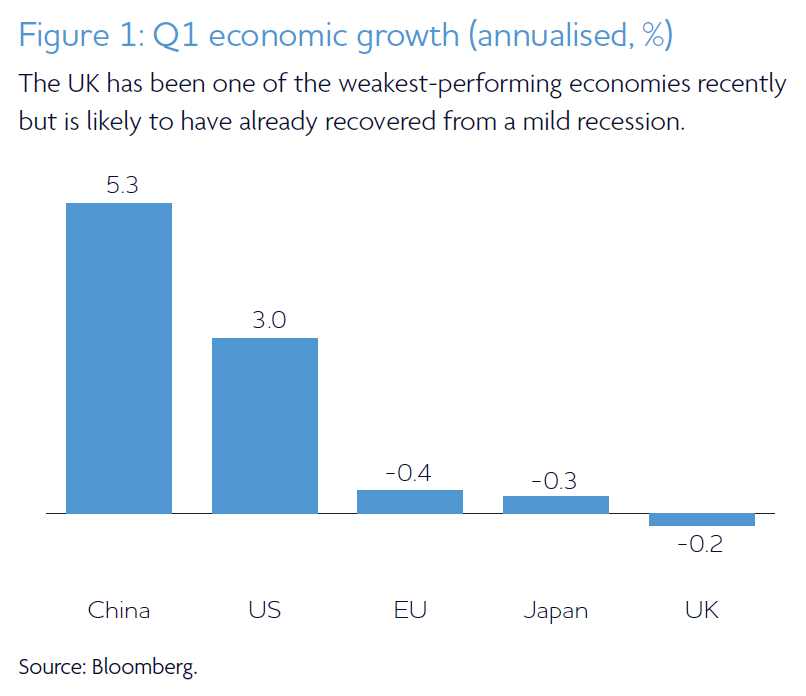

The UK economy grew slightly in February, raising hopes it is on its way out of a recession. UK GDP rose 0.1% in February, boosted by production in manufacturing. It follows growth of 0.3% in January. The jobs market also appears to be cooling, with unemployment nudging up and vacancies dipping.

US inflation unexpectedly rises

Bond and share prices fell after inflation rose 3.5% over the 12 months to March, up from 3.2% in February. The hotter-than-expected inflation report could lower the chances of a summer interest rate cut by the US Federal Reserve (Fed). With the outlook for inflation worsening, consumer sentiment also slipped slightly slipped in March.

Despite US GDP growth slowing to 1.6% in the first quarter, the economy remains robust. US employers added 303,000 jobs in March, while the unemployment rate edged down to 3.8%. In further evidence that the economy ended the first quarter on solid ground, US retail sales also increased more than expected in March.

ECB could cut rates by the summer

Inflation in the euro area fell from 2.6% to 2.4% in March, boosting expectations that the European Central Bank (ECB) will cut interest rates by the summer. European stock markets closed higher after the ECB left interest rates on hold once again at 4% and suggested it could cut rates if its next forecasts show inflation pressures are easing.

The region’s economy is slowly emerging from its slump, with business activity expanding at the fastest pace for almost a year. European private sector economic activity rebounded in April, led by strong demand in services, although manufacturing continued to contract.

Meanwhile, China’s GDP increased at an annual rate of 5.3% in the first quarter, in the latest sign its economy is picking up. Industrial production also increased 6.1% in the first quarter compared with a year earlier, while retail sales expanded 4.7% over the same period.

However, while China’s economy made a stronger than expected start to the year, the property crisis deepened. Property investment fell by 9.5% compared with a year earlier, while new home prices dropped at the fastest pace for more than eight years.

China reported its exports sank 7.5% in March compared with the year before, while imports also fell. Consumer prices also nudged higher by 0.1% in March, underlying the problems the government faces as it seeks to boost domestic demand.

Issued by Omnis Investments Limited. This update reflects Omnis and our investment management firms’ views at the time of writing and is subject to change. The document is for informational purposes only and is not investment advice. We recommend you discuss any investment decisions with your financial adviser. Omnis is unable to provide investment advice. Every effort is made to ensure the accuracy of the information but no assurance or warranties are given. Past performance should not be considered as a guide to future performance.

Issued by Omnis Investments Limited. This update reflects Omnis and our investment management firms’ views at the time of writing and is subject to change. The document is for informational purposes only and is not investment advice. We recommend you discuss any investment decisions with your financial adviser. Omnis is unable to provide investment advice. Every effort is made to ensure the accuracy of the information but no assurance or warranties are given. Past performance should not be considered as a guide to future performance.

The Omnis Managed Investments ICVC and the Omnis Portfolio Investments ICVC are authorised Investment Companies with Variable Capital. The authorised corporate director of the Omnis Managed Investments ICVC and the Omnis Portfolio Investments ICVC is Omnis Investments Limited (Registered Address: Auckland House, Lydiard Fields, Swindon SN5 8UB) which is authorised and regulated by the Financial Conduct Authority.

Approved by Omnis Investments on 2 May 2024.

Essential Wealth Management

1-2 Great Farm Barns

West Woodhay

Newbury

Berkshire RG20 0BP

Tel: 01488 669840

Fax: 01488 669216

Email: [email protected]

Essential Wealth Management is a trading name of Essential Wealth Management and Advice Ltd which is an appointed representative of 2plan wealth management Ltd which is authorised and regulated by the Financial Conduct Authority. Essential Wealth Management and Advice Ltd is entered on the FCA register (www.FCA.org.uk) under no. 518528. Registered office: 1-2 Great Farm Barns, West Woodhay,Newbury, Berkshire RG20 0BP. Registered in England and Wales Number: 04020006.

The Financial Ombudsman Service is available to mediate individual complaints that clients and financial services businesses aren't able to resolve themselves. To contact the Financial Ombudsman Service please visit: http://www.financial-ombudsman.org.uk/contact/index.html

The information on this website is subject to the UK regulatory regime and is therefore targeted at consumers in the UK.

Approved by 2plan wealth management Ltd on 20/05/2025