Nearly all our clients are referred by existing clients, a testament to our service.

In order to ensure we provide our clients with the highest quality and breadth of service, we have a tried and tested team of associated professionals with specific fields of expertise.

Nationwide’s latest research around house affordability for first-time buyers, which, it believes, has improved.

According to the Nationwide, continued improvement in affordability helped support first-time buyer activity over 2025. There remained considerable variation in affordability across occupational groups, with affordability most challenging for people working in sales and customer service, but easier for those in managerial and professional roles. And affordability was most stretched in London and the South of England, while the North and Scotland were the most affordable. It found that a 10% deposit on a typical UK first-time buyer property was around £23k, which, it said, would take nearly six years to save.

Commenting on the figures, Andrew Harvey, Nationwide’s Senior Economist, said:

“With price growth well below the rate of earnings growth and a steady decline in mortgage rates, affordability constraints have eased somewhat over the past year, helping to underpin buyer demand.

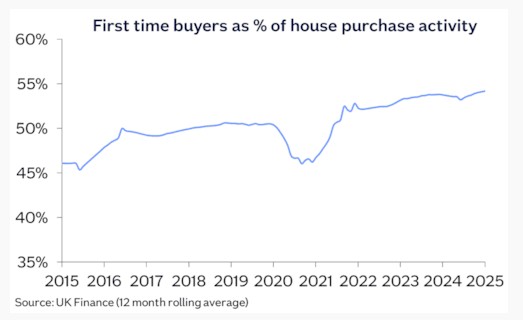

“Indeed, the first-time buyer share of house purchase activity was above the long run average, supported by easier credit availability, with the share of high loan-to-value lending (i.e. with a deposit of 15% or less) reaching its highest level for over a decade. First-time buyer activity over the last year was around 20% higher than 2024 levels.”

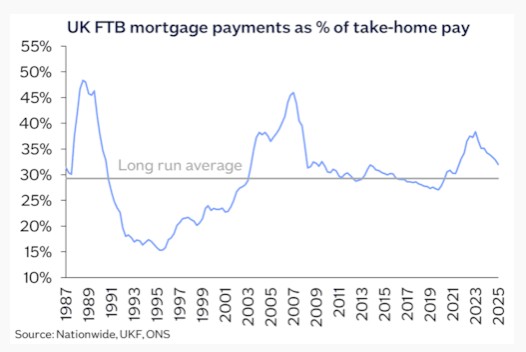

The Nationwide’s main affordability benchmark showed that a prospective buyer earning the average UK income and buying a typical first-time buyer property with a 20% deposit would have a monthly mortgage payment equivalent to 32% of their take-home pay – slightly above the long-run average of 30% and well below the recent high of 48% recorded in 1989.

The Nationwide’s main affordability benchmark showed that a prospective buyer earning the average UK income and buying a typical first-time buyer property with a 20% deposit would have a monthly mortgage payment equivalent to 32% of their take-home pay – slightly above the long-run average of 30% and well below the recent high of 48% recorded in 1989.

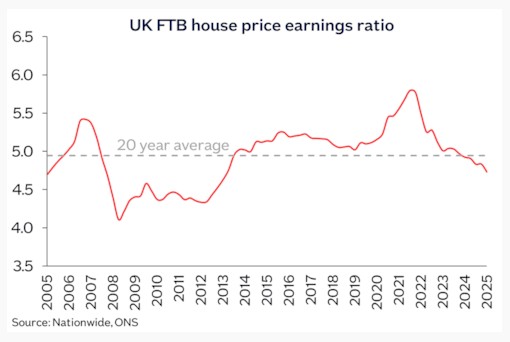

It found that there had also been an improvement in the first-time buyer (FTB) house price to earnings ratio (HPER) to 4.7. This is a continuation of the trend seen over recent years, with the ratio now slightly below its 20-year average. Consequently, commented Mr Harvey, this suggests it is a little easier for prospective buyers to save for a deposit, although it is still particularly challenging for those in the private rented sector, given rental increases in recent years.

It found that there had also been an improvement in the first-time buyer (FTB) house price to earnings ratio (HPER) to 4.7. This is a continuation of the trend seen over recent years, with the ratio now slightly below its 20-year average. Consequently, commented Mr Harvey, this suggests it is a little easier for prospective buyers to save for a deposit, although it is still particularly challenging for those in the private rented sector, given rental increases in recent years.

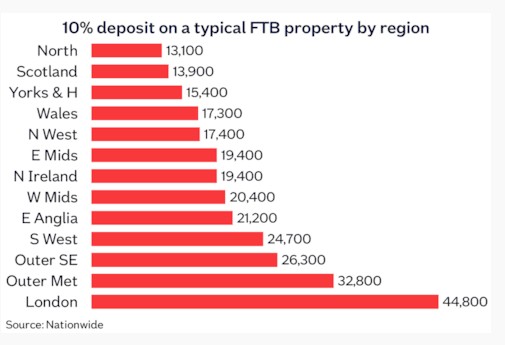

As mentioned above, the Nationwide found that a 10% deposit on a typical UK first-time buyer property is around £23,000, and that, even based on saving 10% of average net pay (c. £320) per month, it would take a prospective buyer nearly six years to accumulate this. However, it added. the level of deposit required also varies considerably by region, reflecting differences in average house prices. For example, a 10% deposit in London is over three times larger than the equivalent in the North (as illustrated below). It would also take a Londoner nine years to save for their deposit versus around four years for someone buying in the North, based on saving 10% of their average net pay.

As mentioned above, the Nationwide found that a 10% deposit on a typical UK first-time buyer property is around £23,000, and that, even based on saving 10% of average net pay (c. £320) per month, it would take a prospective buyer nearly six years to accumulate this. However, it added. the level of deposit required also varies considerably by region, reflecting differences in average house prices. For example, a 10% deposit in London is over three times larger than the equivalent in the North (as illustrated below). It would also take a Londoner nine years to save for their deposit versus around four years for someone buying in the North, based on saving 10% of their average net pay.

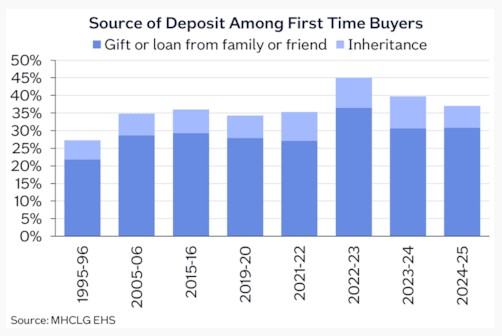

Consequently, the Nationwide concluded, a significant proportion of first-time buyers still have to draw on help from friends and family to raise a deposit, adding that, in 2024/25, over a third of first-time buyers had some assistance raising a deposit, either in the form of a gift or loan from family or friends, or through an inheritance.

Consequently, the Nationwide concluded, a significant proportion of first-time buyers still have to draw on help from friends and family to raise a deposit, adding that, in 2024/25, over a third of first-time buyers had some assistance raising a deposit, either in the form of a gift or loan from family or friends, or through an inheritance.

Mr Harvey added:

Mr Harvey added:

“Looking ahead, we expect housing market activity to strengthen a little further as affordability continues to improve gradually via income growth outpacing house price growth and a further modest decline in interest rates.”

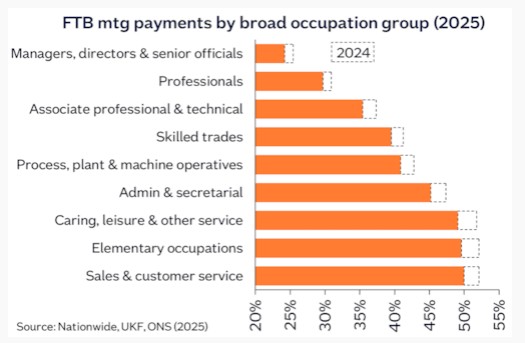

The Nationwide also explored how affordability varies for people in different professions, and found, perhaps unsurprisingly, that mortgage payments relative to take-home pay remained the lowest for those in managerial and professional roles, where average earnings tend to be higher (please see the chart below).

The Nationwide found that all occupations have seen an improvement in affordability since 2024, with the biggest improvement being for those working in caring, leisure and other service occupations, which have seen higher earnings growth.

The Nationwide found that all occupations have seen an improvement in affordability since 2024, with the biggest improvement being for those working in caring, leisure and other service occupations, which have seen higher earnings growth.

It warned that these are benchmark measures, which use the average earnings in each occupational group and the UK typical first-time buyer property price, adding that, in practice, those in higher paid occupations are more likely to purchase more expensive properties.

As mentioned above, the Nationwide found that affordability is most challenging for those working in sales and customer service roles and for those classified as ‘elementary occupations’, which include construction and manufacturing labourers, cleaners and couriers. In these groups, typical mortgage payments would represent around 50% of average take-home pay. The differences in affordability reflecting the divergence in earnings by occupational group. For example, managers, directors and senior officials typically take home around twice as much per year than those working in administrative and secretarial roles.

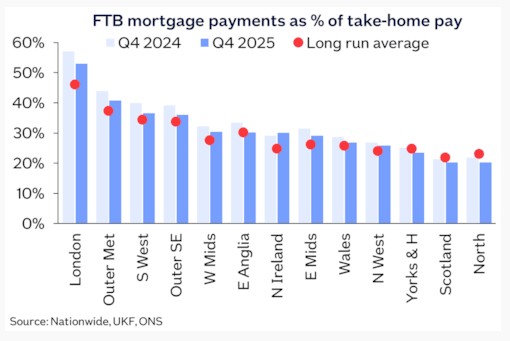

The Nationwide found that all parts of the UK, with the exception of Northern Ireland, have seen a continued improvement in affordability over the past year when looking at the costs of servicing the typical mortgage as a share of take-home pay.

It found that Northern Ireland saw a deterioration in affordability due to the strong house price growth experienced over the past year. And, while mortgage payments as a share of take-home pay are a little lower than the UK average, they are now noticeably above the long-run average in the region.

It found that Northern Ireland saw a deterioration in affordability due to the strong house price growth experienced over the past year. And, while mortgage payments as a share of take-home pay are a little lower than the UK average, they are now noticeably above the long-run average in the region.

For the second year running, London saw the largest improvement in affordability, reflecting relatively weak house price growth in 2025, solid earnings growth and lower interest rates. Nevertheless, the capital remains the least affordable region by a significant margin (please see the chart above). Affordability pressures remain pronounced in the South of England, whilst in the North, Yorkshire & The Humber and Scotland, mortgage payments as a share of take-home pay are actually slightly below their long-run average.

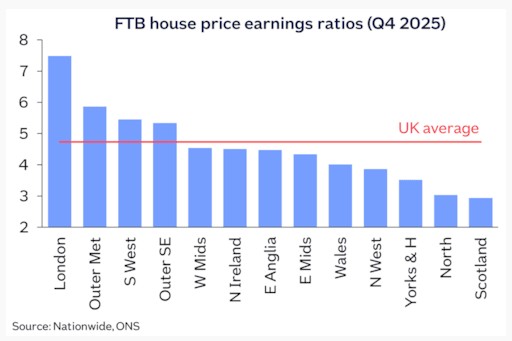

The Nationwide found that most regions have seen a slight improvement in their house price to earnings ratios relative to a year ago, with London continuing to have the highest house price to earnings ratio at 7.5 and Scotland the lowest at 2.9.

The Nationwide found that most regions have seen a slight improvement in their house price to earnings ratios relative to a year ago, with London continuing to have the highest house price to earnings ratio at 7.5 and Scotland the lowest at 2.9.

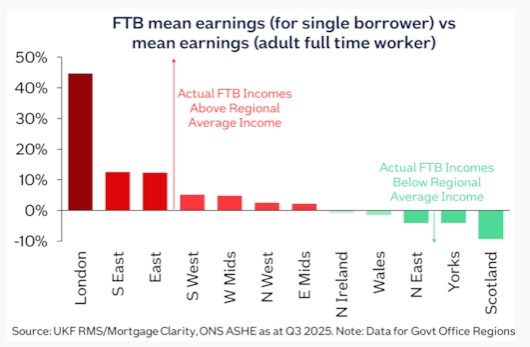

These regional variations in affordability have led to some stark differences emerging between those who would like to buy and those that can do so. To explore this further, the Nationwide looked at how the mean earnings for actual first-time buyers compared to the regional average incomes used in its affordability benchmarks.

Mr Harvey’s concluding comments were that “London stands out as the area with the greatest divergence, with actual first-time buyer earnings (for a single borrower) around 45% higher than average incomes in the capital. But in regions where affordability is less stretched, such as the Midlands, actual first-time buyer earnings tend to be much closer to regional averages. And in a few areas, most notably Scotland, the incomes of actual first-time buyers are below the average income in the region, indicating relatively healthy housing affordability.”

Mr Harvey’s concluding comments were that “London stands out as the area with the greatest divergence, with actual first-time buyer earnings (for a single borrower) around 45% higher than average incomes in the capital. But in regions where affordability is less stretched, such as the Midlands, actual first-time buyer earnings tend to be much closer to regional averages. And in a few areas, most notably Scotland, the incomes of actual first-time buyers are below the average income in the region, indicating relatively healthy housing affordability.”

You can read the full Nationwide report here.

Source: Techlink Professional. This is a news bulletin and is up-to-date as of the date of publishing. Please check the publishing date at the top of the article.

Essential Wealth Management

1-2 Great Farm Barns

West Woodhay

Newbury

Berkshire RG20 0BP

Tel: 01488 669840

Fax: 01488 669216

Email: [email protected]

Essential Wealth Management is a trading name of Essential Wealth Management and Advice Ltd which is an appointed representative of 2plan wealth management Ltd which is authorised and regulated by the Financial Conduct Authority. Essential Wealth Management and Advice Ltd is entered on the FCA register (www.FCA.org.uk) under no. 518528. Registered office: 1-2 Great Farm Barns, West Woodhay,Newbury, Berkshire RG20 0BP. Registered in England and Wales Number: 04020006.

The Financial Ombudsman Service is available to mediate individual complaints that clients and financial services businesses aren't able to resolve themselves. To contact the Financial Ombudsman Service please visit: http://www.financial-ombudsman.org.uk/contact/index.html

The information on this website is subject to the UK regulatory regime and is therefore targeted at consumers in the UK.

Approved by 2plan wealth management Ltd on 20/05/2025