We offer clarity, common sense and total reliability, combined with financial flair.

Markets under pressure.

Global stock markets came under pressure in March amid growing concerns about the economic impact of President Donald Trump’s tariffs. US stocks dropped sharply and bond yields (which means bond prices rose) fell after Trump refused to rule out the possibility that his policies could trigger a recession. Long-threatened tariffs have pushed the country into a trade war, while shifting plans for new levies added to the uncertainty.

Stock market falls, trade tensions and weakening consumer sentiment have reignited fears of a US downturn. The US central bank, the Federal Reserve (Fed), cut its growth forecast, warning that Trump’s tariffs were driving up prices. European bond yields rose on news of increased defence spending, which raised expectations of higher government borrowing and inflation. UK shares also dropped amid uncertainty over US trade policy.

The Fed held interest rates steady but signalled cuts are likely later this year, keeping its key borrowing rate in a range of 4.25% to 4.5%. US inflation came in at 2.8% in February, down from 3% in January. The US labour market has been sluggish, with 151,000 jobs added in February and unemployment rising to 4.1%. Consumer sentiment tumbled in March as long-term inflation expectations reached a 32-year high.

UK inflation edges down

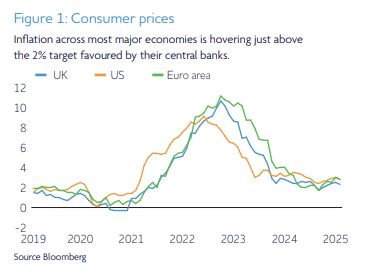

UK inflation fell to 2.8% in February, down from 3% in January. With inflation still elevated, the Bank of England held interest rates at 4.5%. While interest rates have been cut three times since last summer, persistent inflation has raised concerns they may need to stay higher for longer.

Chancellor Rachel Reeves used the Spring Statement to announce major welfare cuts and higher defence spending. The Office for Budget Responsibility forecast economic growth of just 1% in 2025.

Figures showed the economy shrank by 0.1% in January, mainly due to falling manufacturing output. Wage growth remained strong at 5.8%, slightly down on the previous month but still outpacing inflation. Unemployment held steady at 4.4%. On a more positive note, business surveys suggest tentative signs of recovery, driven by financial and consumer services.

EU announces retaliatory tariffs

After Trump imposed 25% tariffs on steel and aluminium imports, the EU responded with duties on €26 billion worth of American goods. The European Central Bank (ECB) cut its deposit rate by a quarter-point to 2.5% and lowered growth forecasts for this year and next amid tariff uncertainty. Euro area inflation fell to 2.3% in February, the first drop in four months. Unemployment remains at a record low, though analysts expect it to rise in the months ahead.

Asia shows signs of resilience

Stronger-than-expected data helped Asian markets as China’s economy showed signs of improvement. Retail sales rose 4% and industrial production climbed 5.9% in January and February. But the housing market remains a drag, with real estate investment down 9.8%. Consumer inflation also fell more than expected, to below zero for the first time in 13 months.

Elsewhere in Asia, Japan’s economy also offered some positive signals, with exports rebounding and business confidence improving. South Korea reported a rise in industrial output, while India’s economy continued to grow steadily, supported by strong domestic demand.

Issued by Omnis Investments Limited. This update reflects Omnis and our investment management firms’ views at the time of writing and is subject to change. The document is for informational purposes only and is not investment advice. We recommend you discuss any investment decisions with your financial adviser. Omnis is unable to provide investment advice. Every effort is made to ensure the accuracy of the information but no assurance or warranties are given. Past performance should not be considered as a guide to future performance.

Issued by Omnis Investments Limited. This update reflects Omnis and our investment management firms’ views at the time of writing and is subject to change. The document is for informational purposes only and is not investment advice. We recommend you discuss any investment decisions with your financial adviser. Omnis is unable to provide investment advice. Every effort is made to ensure the accuracy of the information but no assurance or warranties are given. Past performance should not be considered as a guide to future performance.

The Omnis Managed Investments ICVC and the Omnis Portfolio Investments ICVC are authorised Investment Companies with Variable Capital. The authorised corporate director of the Omnis Managed Investments ICVC and the Omnis Portfolio Investments ICVC is Omnis Investments Limited (Registered Address: Auckland House, Lydiard Fields, Swindon SN5 8UB) which is authorised and regulated by the Financial Conduct Authority.

Approved by Omnis Investments on 2 April 2025

Essential Wealth Management

1-2 Great Farm Barns

West Woodhay

Newbury

Berkshire RG20 0BP

Tel: 01488 669840

Fax: 01488 669216

Email: [email protected]

Essential Wealth Management is a trading name of Essential Wealth Management and Advice Ltd which is an appointed representative of 2plan wealth management Ltd which is authorised and regulated by the Financial Conduct Authority. Essential Wealth Management and Advice Ltd is entered on the FCA register (www.FCA.org.uk) under no. 518528. Registered office: 1-2 Great Farm Barns, West Woodhay,Newbury, Berkshire RG20 0BP. Registered in England and Wales Number: 04020006.

The Financial Ombudsman Service is available to mediate individual complaints that clients and financial services businesses aren't able to resolve themselves. To contact the Financial Ombudsman Service please visit: http://www.financial-ombudsman.org.uk/contact/index.html

The information on this website is subject to the UK regulatory regime and is therefore targeted at consumers in the UK.

Approved by 2plan wealth management Ltd on 20/05/2025