In order to ensure we provide our clients with the highest quality and breadth of service, we have a tried and tested team of associated professionals with specific fields of expertise.

Markets resilient amid Middle East conflict. Stocks surge despite geopolitical uncertainty, with the FTSE 100 and US markets leading the way.

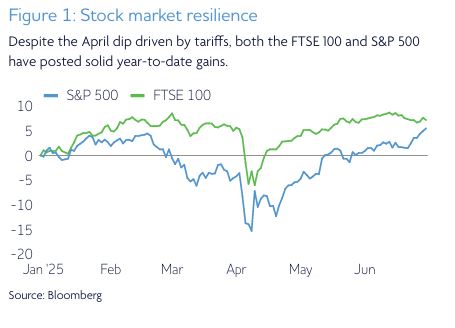

President Trump eases back on tariffs. It was another strong month for global stocks despite rising tensions in the Middle East, with markets shrugging off concerns about the conflict. Brent Crude oil prices rallied above US$80/barrel following US airstrikes on Iran’s nuclear facilities, before retreating towards US$67/barrel after the announcement of a ceasefire. Investor concerns subsequently eased, with fears of an escalation and rising inflation mitigated. Global stocks continued their positive momentum after Trump rolled back on tariffs in May. Meanwhile, the FTSE 100 soared to a record high and the pound hit its highest level against the dollar for more than three years.

US consumer prices continued to rise in May, though not as much as expected despite Trump’s tariffs. Inflation rose 2.4% year-on-year in May, up from 2.3% the previous month. Inflation is expected to rise further as the impact of tariffs is passed on to consumers and businesses. In anticipation of further inflationary pressures the US Federal Reserve (Fed) held borrowing costs between 4.25% and 4.5%. Fed policymakers are expecting two more rate cuts this year.

Whilst the US economy has remained robust, there are now signs it is slowing. The US economy added 139,000 jobs in May, compared with 147,000 jobs added in April. The unemployment rate remained stable at 4.2%, whilst US manufacturing fell for a third straight month after factories were hit by a slump in export orders. Meanwhile, imports tumbled to their lowest level since 2009.

UK stock market surges. The FTSE 100 reached a new record high, close despite the economy shrinking in April. Chancellor Rachel Reeves refused to rule out tax rises after GDP contracted by 0.3%. The f igure was higher than expected and came after Trump’s “Liberation Day” tariffs, tax increases for businesses and a £2 billion monthly plunge in exports to the US. The Bank of England is forecasting GDP growth to slow from 0.7% in the first quarter to 0.25% in the second quarter. The Bank of England held interest rates at 4.25% after inflation remained unchanged from the previous month at 3.4%. Financial markets still expect two rate cuts to 3.75% by the end of this year. Meanwhile, UK unemployment rose to a four-year high of 4.6% in April. Annual pay growth eased to 5.2%.

US and China trade deal. The US agreed on a trade framework with China to boost supplies of rare earth minerals and magnets for the automotive industry, and will raise total tariffs on Chinese goods to 55%. China will impose a 10% tariff on US imports. China’s factory output growth slowed to a six-month low in May, while retail sales picked up, offering some relief for the world’s second largest economy. Industrial production rose 5.8% year-on-year, down from 6.1% in April. In contrast, retail sales grew 6.4%, accelerating from April’s 5.1% rise. Weakness in the Chinese property sector persists, and deflation also remains a concern.

Meanwhile, the European Central Bank (ECB) cut interest rates for the eighth time in a row to 2% in a bid to boost its flagging economy in the wake of Trump’s tariffs. Annual inflation in the eurozone fell to 1.9% in May, down from 2.2% in April and below the ECB’s 2% target Cooling inflation has taken place more rapidly than the ECB predicted earlier this year, partly thanks to a stronger euro, making imported goods cheaper, and lower-than-expected energy costs.

Issued by Omnis Investments Limited. This update reflects Omnis and our investment management firms’ views at the time of writing and is subject to change. The document is for informational purposes only and is not investment advice. We recommend you discuss any investment decisions with your financial adviser. Omnis is unable to provide investment advice. Every effort is made to ensure the accuracy of the information but no assurance or warranties are given. Past performance should not be considered as a guide to future performance.

Issued by Omnis Investments Limited. This update reflects Omnis and our investment management firms’ views at the time of writing and is subject to change. The document is for informational purposes only and is not investment advice. We recommend you discuss any investment decisions with your financial adviser. Omnis is unable to provide investment advice. Every effort is made to ensure the accuracy of the information but no assurance or warranties are given. Past performance should not be considered as a guide to future performance.

The Omnis Managed Investments ICVC and the Omnis Portfolio Investments ICVC are authorised Investment Companies with Variable Capital. The authorised corporate director of the Omnis Managed Investments ICVC and the Omnis Portfolio Investments ICVC is Omnis Investments Limited (Registered Address: Auckland House, Lydiard Fields, Swindon SN5 8UB) which is authorised and regulated by the Financial Conduct Authority. — Approved by Omnis Investments on 1 July 2025.

Essential Wealth Management

1-2 Great Farm Barns

West Woodhay

Newbury

Berkshire RG20 0BP

Tel: 01488 669840

Fax: 01488 669216

Email: [email protected]

Essential Wealth Management is a trading name of Essential Wealth Management and Advice Ltd which is an appointed representative of 2plan wealth management Ltd which is authorised and regulated by the Financial Conduct Authority. Essential Wealth Management and Advice Ltd is entered on the FCA register (www.FCA.org.uk) under no. 518528. Registered office: 1-2 Great Farm Barns, West Woodhay,Newbury, Berkshire RG20 0BP. Registered in England and Wales Number: 04020006.

The Financial Ombudsman Service is available to mediate individual complaints that clients and financial services businesses aren't able to resolve themselves. To contact the Financial Ombudsman Service please visit: http://www.financial-ombudsman.org.uk/contact/index.html

The information on this website is subject to the UK regulatory regime and is therefore targeted at consumers in the UK.

Approved by 2plan wealth management Ltd on 20/05/2025