Nearly all our clients are referred by existing clients, a testament to our service.

With effective planning and support, we can help you achieve your long-term financial goals.

The second quarter of 2025 proved to be a rollercoaster for investors, with markets initially shaken by political developments but ultimately delivering decent returns across both equities and bonds.

A volatile start, followed by recovery

Early in this quarterly review period, on 2nd April, investors were surprised when President Trump spoke in the Rose Garden at the White House, famously wielding a large board listing ‘reciprocal tariffs’ for US trading partners, and introduced a sweeping set of import taxes, sparking a sharp decline in global stock markets.

Investors knew that Trump has for decades been in favour of trade tariffs and he flagged this during his 2024 election campaign, but the scale of these tariffs on what he termed “Liberation Day” caught them off guard. The US stock market dropped more than 10% in just two days, reflecting investor anxiety over the potential economic fallout. However, sentiment improved after a 3-month suspension of these tariffs was announced by President Trump on 9th April, just one week later. This helped markets regain their footing, and by the end of June, the US stock market had not only recovered but reached new highs with a gain of almost 11% in dollar terms for the quarter.

On Monday, President Trump signed an executive order postponing these tariffs for a further 3 weeks to 1st August, removing the focus on the original expiry date which would have been on 9th July.

Geopolitical events and oil market swings

June brought further uncertainty as tensions in the Middle East escalated. Air strikes between Israel and Iran caused oil prices to spike briefly, but a ceasefire agreement soon followed, calming markets. Despite the volatility, oil prices ended the quarter lower, largely due to concerns about slowing global trade.

Economic resilience and easing inflation

Despite the noise, economic indicators remained encouraging. In the US, job creation continued, and inflation data came in softer than expected. In Europe, business sentiment improved, with Germany’s business climate index reaching a one-year high. These developments supported hopes that central banks might lower interest rates later in the year.

Stock markets bounce back

Equities had a good quarter. US shares gained almost 11%, as noted above, in dollar terms and global shares, as measured by the MSCI World Index, rose 5% in sterling terms. Growth-oriented stocks led the way, and emerging markets posted their best quarterly performance in several years, up 12% in dollar terms. In local currency terms Japan’s stock market surged nearly 14% and we saw gains of close to 4% across UK and Europe-ex UK stock indices.

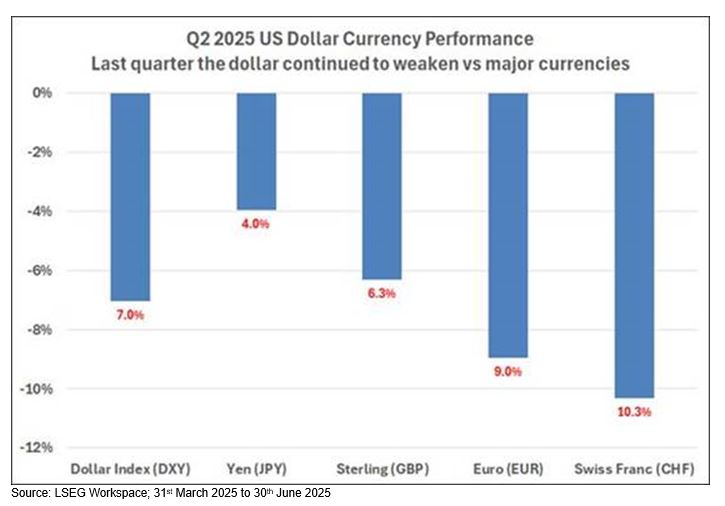

For sterling-based investors, the recent US dollar weakness has adversely impacted US market returns as each dollar effectively “buys less in pounds” when we calculate the stock market performance in sterling terms. The dollar has experienced its worst ‘January to June’ first-half performance since 1973, continuing its decline in the second quarter on concerns about the stability of US economic policies and increased deficits. For example, the “One Big Beautiful Bill” which extends 2017 tax cuts and raises borrowing limits (the debt ceiling) was approved by the US Congress last week and signed into law on Friday 4th July.

The DXY Index, also known as the Dollar Index, measures the value of the US dollar relative to a basket of six major foreign currencies. These are the British pound, Euro, Japanese yen, Canadian dollar, Swedish krona, and Swiss franc. Bond markets hold steady

Bond markets hold steady

Bond investors also saw gains. Although yields initially spiked in response to the tariff news, they later settled down. UK government bonds returned 2%, and European sovereign bonds also posted modest gains. Corporate bonds, especially in Europe, performed well thanks to stable economic data and strong demand. Last week’s uncomfortable scenes of Chancellor Rachel Reeves in tears during Prime Minister’s Questions triggered a brief wobble in UK gilt markets as investors became concerned that her potential departure could lead to a successor more inclined to raise government borrowing, thereby pushing UK interest rates higher. However, the UK’s cost of borrowing (interest paid on government gilts) quickly fell back again; the yield on 30-year gilts stood at 5.287% on 31st March and ended the quarter slightly lower at 5.276%.

Looking ahead

While markets have shown resilience, the outlook remains mixed. Trade disputes, political developments in the US, and geopolitical risks could all lead to further volatility. However, with inflation easing and the possibility of interest rate cuts on the horizon, there are reasons to remain cautiously optimistic. At the time of writing, futures markets are pricing in just over 0.5% of interest rate cuts in the UK between now and the end of this year, which would take our base rate down from 4.25% to 3.75%. In the US, futures pricing is very similar with just under 0.5% of rate cuts expected and this would take the Fed rate down from 4.50% to 4.00% by year-end.

Q2 reporting

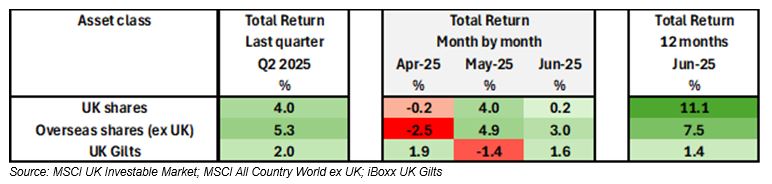

The table below shows how the major asset classes in which we invest, namely UK shares, overseas shares (outside of the UK) and UK gilts, performed last quarter and this is also broken down to show performance in each of the constituent months. Over the next week, we will be dispatching your quarterly investment summary report for the period ending 30th June. The quarterly report will include a valuation of your holdings, a transaction history showing all purchases and sales for the quarter, and a performance comparison against the agreed reference benchmark.

Over the next week, we will be dispatching your quarterly investment summary report for the period ending 30th June. The quarterly report will include a valuation of your holdings, a transaction history showing all purchases and sales for the quarter, and a performance comparison against the agreed reference benchmark.

Source: Quilter Cheviot

Issued by the Quilter Group of companies which comprises Quilter plc and any subsidiary of Quilter plc from time to time. Further details about the Quilter Group are available at https://plc.quilter.com/corporate-and-regulatory-information/ . Quilter plc is registered in England and Wales under number 06404270. Registered Office at Senator House, 85 Queen Victoria Street, London, EC4V 4AB, United Kingdom.

Essential Wealth Management

1-2 Great Farm Barns

West Woodhay

Newbury

Berkshire RG20 0BP

Tel: 01488 669840

Fax: 01488 669216

Email: [email protected]

Essential Wealth Management is a trading name of Essential Wealth Management and Advice Ltd which is an appointed representative of 2plan wealth management Ltd which is authorised and regulated by the Financial Conduct Authority. Essential Wealth Management and Advice Ltd is entered on the FCA register (www.FCA.org.uk) under no. 518528. Registered office: 1-2 Great Farm Barns, West Woodhay,Newbury, Berkshire RG20 0BP. Registered in England and Wales Number: 04020006.

The Financial Ombudsman Service is available to mediate individual complaints that clients and financial services businesses aren't able to resolve themselves. To contact the Financial Ombudsman Service please visit: http://www.financial-ombudsman.org.uk/contact/index.html

The information on this website is subject to the UK regulatory regime and is therefore targeted at consumers in the UK.

Approved by 2plan wealth management Ltd on 20/05/2025