With effective planning and support, we can help you achieve your long-term financial goals.

In order to ensure we provide our clients with the highest quality and breadth of service, we have a tried and tested team of associated professionals with specific fields of expertise.

Iran attack

We summarise events in the Middle East, with thoughts about what might happen next and the consequences for financial markets and your investments. This is a fast-moving situation, so please keep in mind any future developments as the media reports them.

What do we know so far? On Saturday, the US and Israel launched missile attacks on Iran, which continued into Sunday and Monday. A primary target was Iran’s Supreme Leader, Ayatollah Ali Khamenei, whose death has been confirmed. Iran has retaliated by launching its own missiles into neighbouring countries.

However, the impact of this counter attack appears limited: defence systems are reported to have dealt with the bulk of the threat. The highest profile target has been Dubai. Air travel to and from the region has been severely disrupted.

What happens next? The path of action so far suggests a deliberate plan to trigger regime change in Iran, at a time when the country is weak and vulnerable. Mainstream media has plenty of coverage of celebrating expatriate Iranians – and some from within Iran. However, Sunday saw more evidence of pro-government rallies and the mourning of Khamenei.

Recent anti-government protests, before Saturday’s attack, have been severely dealt with, with deaths reported in the tens of thousands. With the existing regime potentially on its last legs, there is, regrettably, the risk of much more violence.

As far as we can see, there is no coherent US plan for what comes next. That opens up the possibility of a protracted civil war. It seems probable that US President Donald Trump was emboldened by a couple of things. One was the swift resolution to his last intervention in Iran, in the summer. Another was the success of the operation to extract President Nicolás Maduro from Venezuela.

The fact that the attacks were launched early on Saturday even suggests that Trump might have hoped to have everything wrapped up by Monday morning, when markets opened. He’s highly attuned to market performance and the resilience of the US economy is, to some degree, dependent upon increases in personal wealth. He’s also fighting a cost-of-living crisis that would only be exacerbated by higher energy prices.

But this situation looks far more complicated than something that can be resolved over a weekend. We should be prepared for a longer period of uncertainty – and pleasantly surprised if there’s a bloodless transition of power to less extreme leadership with limited disruption.

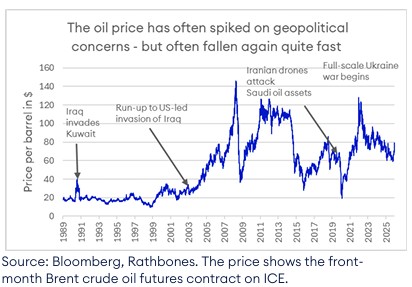

The importance of oil

In the final reckoning, though, it all comes down to oil. The scenarios have been well rehearsed in recent years, and market participants are all aware of the significance of the Strait of Hormuz, the narrow body of water between Iran and Oman.

While Iran itself is a major producer of crude oil, accounting for around 3% of global production, it’s widely agreed that any loss of Iranian oil could be easily accommodated through existing stockpiles and increased Opec production. The major buyer of Iranian crude is China, which has, perhaps in anticipation of such events, been recently increasing its own strategic reserves. China has at least some vested interest in keeping production on tap and could be a party to future negotiations.

The much bigger threat comes from the suspension of cargo deliveries through the Strait. Around 20% of the world’s supply of oil is transported through the Strait from Middle Eastern producers to global consumers. Even after allowing for inventories and strategic reserves, the price of crude oil is, like any commodity, sensitive to even small swings in the balance of supply and demand. Taking 20% of supply out of the equation would be extremely damaging.

Oil traders had been anticipating escalation in the last few weeks, as the US built up its forces in the region. The price of Brent crude has risen from around $60 per barrel, its lowest in almost five years, to close on Friday at $73. This compares to a brief peak of $80 last summer. The high associated with Russia’s full-scale invasion of Ukraine was close to $130. Risk of a relatively short blockade of the Strait could see the short-term oil price jump up to the $80-100 range.

The greater risk is of a much longer closure, from Iran laying mines in the Strait. This could therefore persist long after the current regime has been toppled. One report suggests that Iran has as many as 5,000 radar-controlled mines. There’s no intelligence yet to suggest that they have been. But shipping has been effectively suspended for now, owing to the risk. Insurance brokers are raising the cost of premiums or cancelling policies, for ships travelling through the Strait.

A prolonged closure of the Strait could, according to some analysts, see the oil price rise well above $100. However, we see more alarmist targets of $200-plus as unrealistic. The destruction of demand for oil at that level would be so great that we believe such a price to be unsustainable. It would also make other energy sources more attractive on a relative price basis. Even so, on average, energy costs would rise substantially.

As markets digested the news on Monday morning UK time, the price of Brent crude oil soared as high as 13%, before falling back somewhat to trade, by mid-morning, 8.5% up on Friday's close, at $79.40.

Market implications of Iran strike: equities

Market implications of Iran strike: equities

What, then, are the immediate implications for financial markets? At the highest level, we can expect an initial ‘risk off’ response, where investors seek less risky assets.

Remember that any spike in implied volatility – market expectations of future volatility – forces the immediate reduction of positions by investors whose asset allocation and leverage (the degree to which debt fuels their market positions) is driven by volatility. The Vix, often known as the US stock market’s ‘fear gauge’ because it measures expected volatility in the S&P 500, closed bang on its long-term average of 20 on Friday.

Without wishing to sound too alarming, we should also note that the US market is set up for a rapid unwinding of the popular ‘dispersion trade’ that’s been depressing the volatility of the S&P 500. This involves trading on the gap between the relatively subdued daily move of S&P 500 as a whole, and the large price swings for individual companies. If this gap falls, speculators will have to sell out of these positions.

These factors could cause markets to overshoot to the downside in the short term. But should be more manageable if we understand the mechanisms at work.

Even before the recent attacks, there were signs of investor nervousness, which could fuel volatility. We note the recent gyrations in the technology sector. There are also concerns about the impact on society, including the labour market, of AI.

There’s the sell-off of the US KBW Banks Index on Friday, down 5% on worries about the quality of loans to the private credit sector. This consists of non-bank businesses, such as private equity firms, that provide lending.

More constructively, the market has been aware of this threat for some time, as observed in the rising oil price. So, to some degree, the impact could be mitigated.

Within equities, we can expect to see strong relative outperformance for oil majors and defence stocks. Other safe havens, such as consumer staples, should also be more resilient. Much higher energy prices could undermine the economic case for the build-out of data centres. So, it’s reasonable to expect some profit taking in the names of beneficiaries of the AI capital spending (capex) boom – and there’s a lot of profit to be taken, given the sharp rise in the price of these stocks.

Early in the European trading day on Monday, the Stoxx Europe 600 benchmark index was down 1.8%.

Market implications: bonds

It’s harder to assess the impact on bond markets. Safe haven demand should be supportive, but higher oil prices drive up inflation and there’s an almost unbreakable link between oil prices and inflation expectations. That puts upward pressure on bond yields, especially if the risk of lower GDP growth increases fiscal concerns. On the other hand, and cognizant of the European Central Bank’s mistake in raising interest rates in 2008 in the face of higher oil prices, central banks could well respond with rate cuts. That outcome would support our current favouring of shorter-duration bonds.

Market implications: diversifiers

The other pillar of asset allocation is our diversifiers. Precious metals, mainly gold, should benefit. Actively managed funds that specialise in taking convex exposure to tail risks – generating big pay-offs if markets show particularly extreme negative reactions – should also do well in this environment. Higher overall volatility can produce attractive trading opportunities for the fleet of foot. By mid-morning, gold was up 1.6% to $5,362 a troy ounce.

Diversification will help protect clients

In summary, investors should be prepared for increased volatility in markets and individual securities, but everything is subject to further news as the story unfolds.

However, geopolitical risk is built into our long-term asset allocation, which provides some resilience in these circumstances. Shorter-duration bonds and diversifying assets in particular stand to be good preservers of capital. Our broadly diversified equity exposure doesn’t leave us overexposed to any particular outcome. History shows that knee-jerk selling reactions tend not to lead to the best outcomes for longer-term portfolio investors. It will be short-term traders, especially those utilising leverage who are most exposed and will need to liquidate positions. Even so, every such episode has to be considered on its individual merits and with reference to other factors. We’ll make further assessments and keep you updated as the situation develops.

The value of investments can go down as well as up and you could get back less than you invested. Past performance is not a reliable indicator of future performance. This information should not be taken as financial advice or a recommendation.

Source: Rathbones

Rathbones, Greenbank and Rathbones Financial Planning are a trading names of Rathbones Investment Management Limited, which is authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority. Registered office: Port of Liverpool Building, Pier Head, Liverpool L3 1NW. Registered in England No. 01448919.

Essential Wealth Management

1-2 Great Farm Barns

West Woodhay

Newbury

Berkshire RG20 0BP

Tel: 01488 669840

Fax: 01488 669216

Email: [email protected]

Essential Wealth Management is a trading name of Essential Wealth Management and Advice Ltd which is an appointed representative of 2plan wealth management Ltd which is authorised and regulated by the Financial Conduct Authority. Essential Wealth Management and Advice Ltd is entered on the FCA register (www.FCA.org.uk) under no. 518528. Registered office: 1-2 Great Farm Barns, West Woodhay,Newbury, Berkshire RG20 0BP. Registered in England and Wales Number: 04020006.

The Financial Ombudsman Service is available to mediate individual complaints that clients and financial services businesses aren't able to resolve themselves. To contact the Financial Ombudsman Service please visit: http://www.financial-ombudsman.org.uk/contact/index.html

The information on this website is subject to the UK regulatory regime and is therefore targeted at consumers in the UK.

Approved by 2plan wealth management Ltd on 20/05/2025