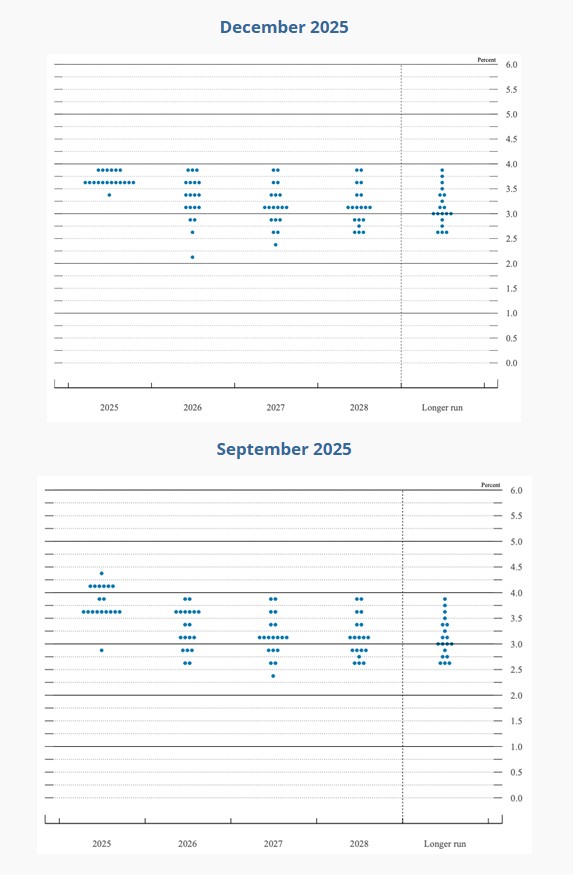

On Wednesday, the Federal Reserve cut the Fed Funds to 3.75%-3.50%, as had been widely anticipated. More interesting was the dot plot which accompanied the announcement.

The Federal Reserve’s last meeting of 2025 produced the third consecutive 0.25% cut of the year, to 3.50%-3.75%. The vote for the cut was 9-3, with two dissents favouring no change and Donald Trump’s latest appointee, Steve Miran, again out on a limb calling for a 50 basis points reduction. Next year promises to be an interesting one for the Fed:

The Federal Reserve’s last meeting of 2025 produced the third consecutive 0.25% cut of the year, to 3.50%-3.75%. The vote for the cut was 9-3, with two dissents favouring no change and Donald Trump’s latest appointee, Steve Miran, again out on a limb calling for a 50 basis points reduction. Next year promises to be an interesting one for the Fed:

Early in 2026, Donald Trump will announce the new Fed chair, to replace Jay Powell when his term expires in May. There has been no love lost between Trump and the man he appointed during his first presidential term, but whom Trump now regularly calls Mr Too Late and last night labelled “a stiff”. The betting markets currently have Kevin Hasset, director of the National Economic Council and a Trump supporter, as the most likely replacement.

While Trump will demand that the new chair cuts rates faster to juice the economy ahead of November’s mid-term elections, he may not get his way. There are 12 voting members of the Fed’s rate setting Federal Open Market Committee (FOMC), so even with three Trump-appointed members and the chair, FOMC votes could go against The Donald’s wishes. As mentioned above, Wednesday’s vote produced only on (Trump-nominated) member calling for a 50 basis point cut.

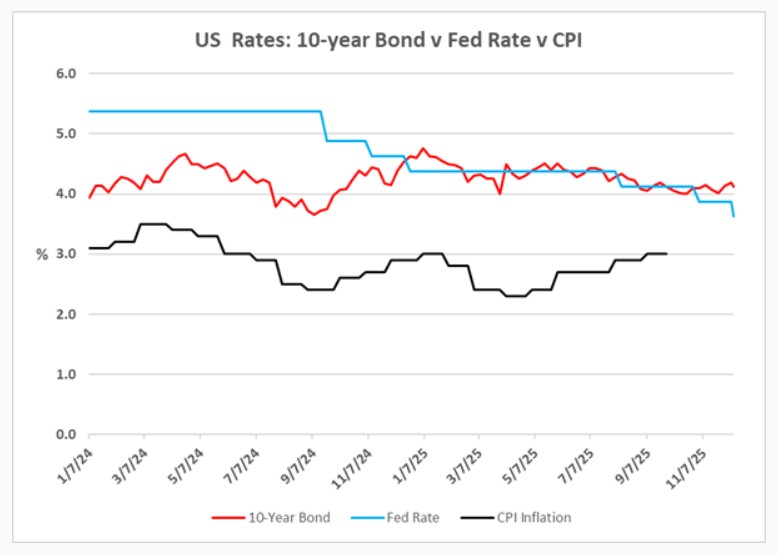

As the graph shows, the 1.75 percentage points which have been lopped from the Fed funds rate since September 2024 have been accompanied by an increase in the 10-year Treasury bond yield of close to 50 basis points. That can be read in a variety of ways, but none suggest rates are heading down and staying down.

Buried in the weeds of Wednesday’s Fed announcements was the statement that the Fed would be buying $40bn of Treasury Bills in December and that purchases in the following months would be a similar levels. These purchases were presented as being made largely for technical reasons, but some commentators saw them as an indicator that the Fed was returning to quantitative easing to manage interest rates in 2026.

Inflation is proving to be sticky – the Fed statement notes that inflation “remains somewhat elevated”. The US government shutdown means the last official CPI reading is 3% for September and November’s figure will not appear until 18 December. The Bureau of Labour Statistics will not calculate an official October figure because it is impractical to obtain the necessary data. Trump is under pressure on ‘affordability’, an issue he used to defeat Biden, so he needs the CPI readings to drop. Economic theory (if not Trump’s) says countering inflation means not reducing interest rates.

The Fed’s move to 3.75%-3.50%, had been widely anticipated. This meeting accompanied by the final dot-plot of the year (see below) showing Fed members’ projections of future interest rates. At first (or even second) glance, you could be forgiven for thinking nothing had changed. The median projections for interest rates are indeed unaltered, although other projections show the Fed more optimistic about GDP growth in 2026 than it was in September (2.3% against 1.8%) and marginally less pessimistic about 2026 inflation (core PCE at 2.5% rather than 2.6%, which is still above target).

One unmentioned cloud on the near horizon is the Supreme Court decision on the legality of Trump’s tariffs. These have mostly been imposed under the International Emergency Economic Powers Act (IEEPA) 1977, an act designed to allow a president to control international economic transactions in a period of a declared national emergency threatening U.S. security or economy. IEEPA contains no explicit reference to tariffs, which historically have been the province of Congress, not the White House. The current consensus is that Trump will lose at the Supreme Court (the betting markets give him roughly a one in four chance of victory). A defeat could upend US government finances, forcing refunds of tariffs already collected and an even wider budget deficit to be financed until replacement levies are put into effect.

Source: Techlink Professional

Source: Techlink Professional

This is a news bulletin and is up-to-date as of the date of publishing. Please check the publishing date at the top of the article.

Essential Wealth Management

1-2 Great Farm Barns

West Woodhay

Newbury

Berkshire RG20 0BP

Tel: 01488 669840

Fax: 01488 669216

Email: [email protected]

Essential Wealth Management is a trading name of Essential Wealth Management and Advice Ltd which is an appointed representative of 2plan wealth management Ltd which is authorised and regulated by the Financial Conduct Authority. Essential Wealth Management and Advice Ltd is entered on the FCA register (www.FCA.org.uk) under no. 518528. Registered office: 1-2 Great Farm Barns, West Woodhay,Newbury, Berkshire RG20 0BP. Registered in England and Wales Number: 04020006.

The Financial Ombudsman Service is available to mediate individual complaints that clients and financial services businesses aren't able to resolve themselves. To contact the Financial Ombudsman Service please visit: http://www.financial-ombudsman.org.uk/contact/index.html

The information on this website is subject to the UK regulatory regime and is therefore targeted at consumers in the UK.

Approved by 2plan wealth management Ltd on 20/05/2025