Why the Office for Budget Responsibility (OBR) will be considering the impact of high marginal tax rates in the coming months

In last week’s Economic and Fiscal Outlook (EFO), under the broad heading of Specific Risks, the OBR said:

“The tax-to-GDP ratio is forecast to increase to a post-war high of 38.5 per cent of GDP in 2030/31. And many marginal tax rates – of relevance to incentives to work, save and invest – are much higher. A higher level of the tax take increases the risk that incentives within the tax system distort or constrain economic activity by more than expected. For example, capital taxes are paid by a narrow base of typically higher-income taxpayers and are often very sensitive to the behavioural responses to policy changes. The yield from the personal tax threshold freezes across the forecast is very sensitive to future inflation and nominal earnings growth.”

The OBR’s concern about marginal rates appears elsewhere in the EFO, with a promise of future research:

“While the level of the tax take in the UK is not unusually high compared to other advanced economies, there is some evidence that UK marginal rates of tax may be above the OECD average and this may be more relevant for impacts on incentives to work, save, and invest. We plan to conduct further analysis of UK marginal tax rates relative to other countries in our upcoming 2026 Fiscal risks and sustainability report.”

The OBR’s promised investigation comes at a time when the issues caused by the £100,000 tax threshold/cliff are gaining media attention. As a reminder, at £100,000 of adjusted net income:

The personal allowance starts to be phased out across the next £25,140 of income, creating an effective marginal income tax rate of up to 60% (67.5% in Scotland);

Entitlement to tax-free childcare, worth up to £2,000 per child is lost; and

Outside Scotland, some or all entitlement to free childcare is lost.

Add in 2% National Insurance on earnings and, for some graduates, 9% student loan repayment and it is easy to see why there are stories of people refusing promotion or cutting back on working hours to avoid hitting the six-figure income threshold. Three years ago, responding to childcare reforms in the Spring 2023 Budget, the Institute for Fiscal Studies gave the following examples of the impact of the £100,000 threshold:

A parent with two children under 3 whose childcare provider charges England’s [2023] average hourly rate for 40 hours per week would … find that their disposable income (i.e., earnings net of tax and childcare outgoings) falls by £14,500 if their pre-tax pay crosses £100,000. Disposable income would not recover its previous level until pre-tax pay reached £134,500, meaning a parent earning £130,000 would be worse off than one earning £99,000.

For those with higher childcare costs the distortions are even more absurd. A similar parent paying average [2023] London rates for childcare, using 50 hours per week, would see a £20,000 fall in disposable income when their pre-tax earnings cross £100,000. Disposable income would not recover its previous level until pre-tax pay reached £144,500.

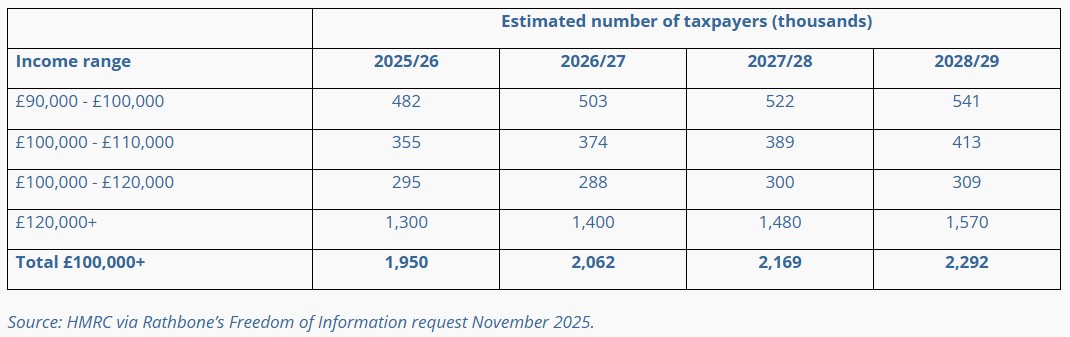

The £100,000 threshold may sound academic when Average Weekly Earnings are about £38,000 a year, but HMRC’s response to a Freedom of Information request from Rathbones shows the number of people affected is significant:

According to the latest HMRC projections, about £1 in every £8 of income tax comes from those with income in the £100,000-£150,000 band, almost as much as from their higher earning counterparts in the £200,000-£500,000 band.

According to the latest HMRC projections, about £1 in every £8 of income tax comes from those with income in the £100,000-£150,000 band, almost as much as from their higher earning counterparts in the £200,000-£500,000 band.

It is hard to imagine that Rachel Reeves will pay much heed to what the OBR research reveals. The issue of disincentivising marginal rates has been around for many years and correcting it would either be expensive or involve a major restructuring of income tax, probably with increased rates at lower levels than now.

Source: Techlink Professional. This is a news bulletin and is up-to-date as of the date of publishing. Please check the publishing date at the top of the article.

Essential Wealth Management

1-2 Great Farm Barns

West Woodhay

Newbury

Berkshire RG20 0BP

Tel: 01488 669840

Fax: 01488 669216

Email: [email protected]

Essential Wealth Management is a trading name of Essential Wealth Management and Advice Ltd which is an appointed representative of 2plan wealth management Ltd which is authorised and regulated by the Financial Conduct Authority. Essential Wealth Management and Advice Ltd is entered on the FCA register (www.FCA.org.uk) under no. 518528. Registered office: 1-2 Great Farm Barns, West Woodhay,Newbury, Berkshire RG20 0BP. Registered in England and Wales Number: 04020006.

The Financial Ombudsman Service is available to mediate individual complaints that clients and financial services businesses aren't able to resolve themselves. To contact the Financial Ombudsman Service please visit: http://www.financial-ombudsman.org.uk/contact/index.html

The information on this website is subject to the UK regulatory regime and is therefore targeted at consumers in the UK.

Approved by 2plan wealth management Ltd on 20/05/2025