Our holistic approach, combined with an insightful understanding of the worlds of finance, law, taxation, investment and insurance, ensures all your bases are covered.

LCP’s paper explaining “Why raiding pension tax relief is riskier than it looks”

LCP (Lane Clark & Peacock), where the former Pensions Minister Steve Webb is now a partner, has issued a report entitled “How to avoid an ‘Omnishambles’ Budget”. Arguably, Steve Webb, one of the report’s authors, is in a prime position to give advice on the subject as he was a member of the 2010-15 Coalition Government at the time when George Osborne presented the infamous ‘pasty-tax’ Budget.

Unsurprisingly, Steve Webb and his colleagues’ focus is not now on static caravans, but the potential impacts of a Budget raid on pensions. This is seen as targeted on three possible areas:

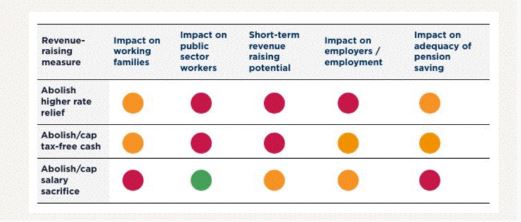

Scrapping higher rates of tax relief enjoyed by those who pay tax above the basic rate,

Capping (or even scrapping) the ability to take 25% of a pension as a tax-free lump sum,

Capping or scrapping salary sacrifice for pension contributions, following on from the publication earlier this year of HMRC research into employer responses to theoretical reforms.

LCP sets out five potential ‘traps for the unwary’ [Chancellor] which could be linked to some or all of the trio of changes:

Breaking the manifesto commitment that “Labour will not increase taxes on working people.”

Hitting the public sector, which in many sectors has high contribution rates, especially hard at a time of fragile industrial relations.

Failure to raise meaningful money in this Parliament. Remember, this Budget must meet “ironclad” fiscal targets in 2029/30.

The LCP paper notes that “Abolishing higher rate relief would be a major structural change to the pension system, requiring lengthy consultation with pension schemes and providers and employers, complex legal changes to implement a new system and considerable time to change administration and payroll systems to reflect the new rules, because of the time taken to implement change or because of the need for extensive protection for losers.”

Similarly, it suggests “Capping tax-free cash would be widely seen as ‘moving the goalposts’ for those who were approaching retirement” and, as a result, would require “extensive transitional protections…[meaning] that extra revenue from this measure could be negligible in this Parliament.”

Putting extra burdens on employers, coming on top of the £25bn hike in employer national insurance (NICs) in the 2024 Budget. This is, arguably, a little disingenuous as one oft-unmentioned aspect of the NICs increase was that compensation (£5.5bn in 2025/26) was provided to public sector employers and adult social care. The £25bn figure ignores this.

Undermining pension saving, at a time when even the Government estimates that around 14 million workers are not saving enough for a decent retirement.

LCP summarises the risks in a traffic light chart:

Source: Techlink Professional

Source: Techlink Professional

This is a news bulletin and is up-to-date as of the date of publishing. Please check the publishing date at the top of the article.

Essential Wealth Management

1-2 Great Farm Barns

West Woodhay

Newbury

Berkshire RG20 0BP

Tel: 01488 669840

Fax: 01488 669216

Email: [email protected]

Essential Wealth Management is a trading name of Essential Wealth Management and Advice Ltd which is an appointed representative of 2plan wealth management Ltd which is authorised and regulated by the Financial Conduct Authority. Essential Wealth Management and Advice Ltd is entered on the FCA register (www.FCA.org.uk) under no. 518528. Registered office: 1-2 Great Farm Barns, West Woodhay,Newbury, Berkshire RG20 0BP. Registered in England and Wales Number: 04020006.

The Financial Ombudsman Service is available to mediate individual complaints that clients and financial services businesses aren't able to resolve themselves. To contact the Financial Ombudsman Service please visit: http://www.financial-ombudsman.org.uk/contact/index.html

The information on this website is subject to the UK regulatory regime and is therefore targeted at consumers in the UK.

Approved by 2plan wealth management Ltd on 20/05/2025