Our holistic approach, combined with an insightful understanding of the worlds of finance, law, taxation, investment and insurance, ensures all your bases are covered.

Market performance. The second week of US/Israel-Iran war saw continued equity market falls, but much less than in week one. However, bonds remained under heavy pressure.

The second week of what some commentators are calling the Third Gulf War was marked by more volatility in equity markets. Many rallied on Tuesday in response to Donald Trump’s remark on Monday that “I think the war is very complete, pretty much.” Thereafter, as war rolled on, markets fell, cancelling out the Trump bump. As the table shows, the net result was generally another week of falls, albeit smaller than in the first week of March.

The second week of what some commentators are calling the Third Gulf War was marked by more volatility in equity markets. Many rallied on Tuesday in response to Donald Trump’s remark on Monday that “I think the war is very complete, pretty much.” Thereafter, as war rolled on, markets fell, cancelling out the Trump bump. As the table shows, the net result was generally another week of falls, albeit smaller than in the first week of March.

Over the second week of the war, the price of Brent Crude followed an inverse pattern to equities, falling on Trump’s statement and then rising for the remainder of the week to close 10.5% up at just over $103 a barrel. On 27 February, it was $72.48. For investors, the combination of the spiralling oil price and the fading hopes of any rapid resolution has raised the spectre of the return of inflation.

After the hard lessons of the Ukraine war, central banks are less likely to look through the inflation spike caused by higher oil prices. In the US that means rate cuts are off the table, while, for Europe and the UK, rate rises are now seen as on the agenda. By coincidence, this week will see meetings of the US, UK, Eurozone and Japanese central banks. The quartet’s deliberations will receive particular attention, although none is expected to raise rates.

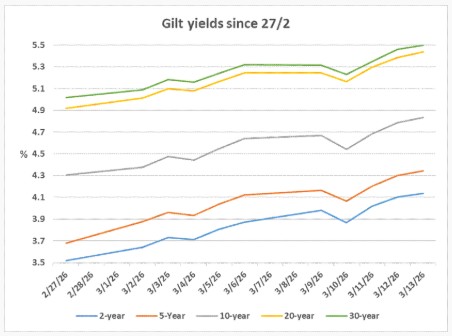

Meanwhile, in the UK, investors are already building rate rises into gilt yields, as the graph below shows:

The most notable moves are at the short end, with two-year yields up 0.62% from 27/2 and five-year yields 0.66% higher. That is not good news for the Chancellor as she has £252bn of gilts to sell in 2026/27, with about 40% of sales earmarked for short-dated stock. A rising bank base rate will also hurt Government finances, given it sets the cost of funding the Bank of England’s still large (£550bn) holding of gilts acquired under QE. A third twist is that higher inflation will boost the revaluation cost to the Exchequer of £700bn of index-linked gilts, just when the (pre-war) forecasts had been for CPI finally to hit its 2% target.

The most notable moves are at the short end, with two-year yields up 0.62% from 27/2 and five-year yields 0.66% higher. That is not good news for the Chancellor as she has £252bn of gilts to sell in 2026/27, with about 40% of sales earmarked for short-dated stock. A rising bank base rate will also hurt Government finances, given it sets the cost of funding the Bank of England’s still large (£550bn) holding of gilts acquired under QE. A third twist is that higher inflation will boost the revaluation cost to the Exchequer of £700bn of index-linked gilts, just when the (pre-war) forecasts had been for CPI finally to hit its 2% target.

Source: Techlink Professional. This is a news bulletin and is up-to-date as of the date of publishing. Please check the publishing date at the top of the article.

Essential Wealth Management

1-2 Great Farm Barns

West Woodhay

Newbury

Berkshire RG20 0BP

Tel: 01488 669840

Fax: 01488 669216

Email: [email protected]

Essential Wealth Management is a trading name of Essential Wealth Management and Advice Ltd which is an appointed representative of 2plan wealth management Ltd which is authorised and regulated by the Financial Conduct Authority. Essential Wealth Management and Advice Ltd is entered on the FCA register (www.FCA.org.uk) under no. 518528. Registered office: 1-2 Great Farm Barns, West Woodhay,Newbury, Berkshire RG20 0BP. Registered in England and Wales Number: 04020006.

The Financial Ombudsman Service is available to mediate individual complaints that clients and financial services businesses aren't able to resolve themselves. To contact the Financial Ombudsman Service please visit: http://www.financial-ombudsman.org.uk/contact/index.html

The information on this website is subject to the UK regulatory regime and is therefore targeted at consumers in the UK.

Approved by 2plan wealth management Ltd on 20/05/2025